Saving money consistently is one of the most important habits for achieving financial stability and long-term success. Whether you’re trying to build an emergency fund, pay off debt, invest for the future, or simply gain more control over your finances, learning how to save money every month can make a significant difference.

The good news is that saving money doesn’t require a high income. With the right strategies and disciplined habits, anyone can improve their financial situation and grow their savings over time.

In this guide, we’ll explore practical and effective ways to save money every month and build a stronger financial future.

Why Saving Money Matters

Many people live paycheck to paycheck and struggle to prepare for unexpected expenses. Regular savings provide financial security and help you:

- Handle emergencies

- Reduce financial stress

- Achieve personal goals

- Invest for the future

- Avoid unnecessary debt

- Build long-term wealth

Even small monthly savings can grow significantly through consistency and smart financial planning.

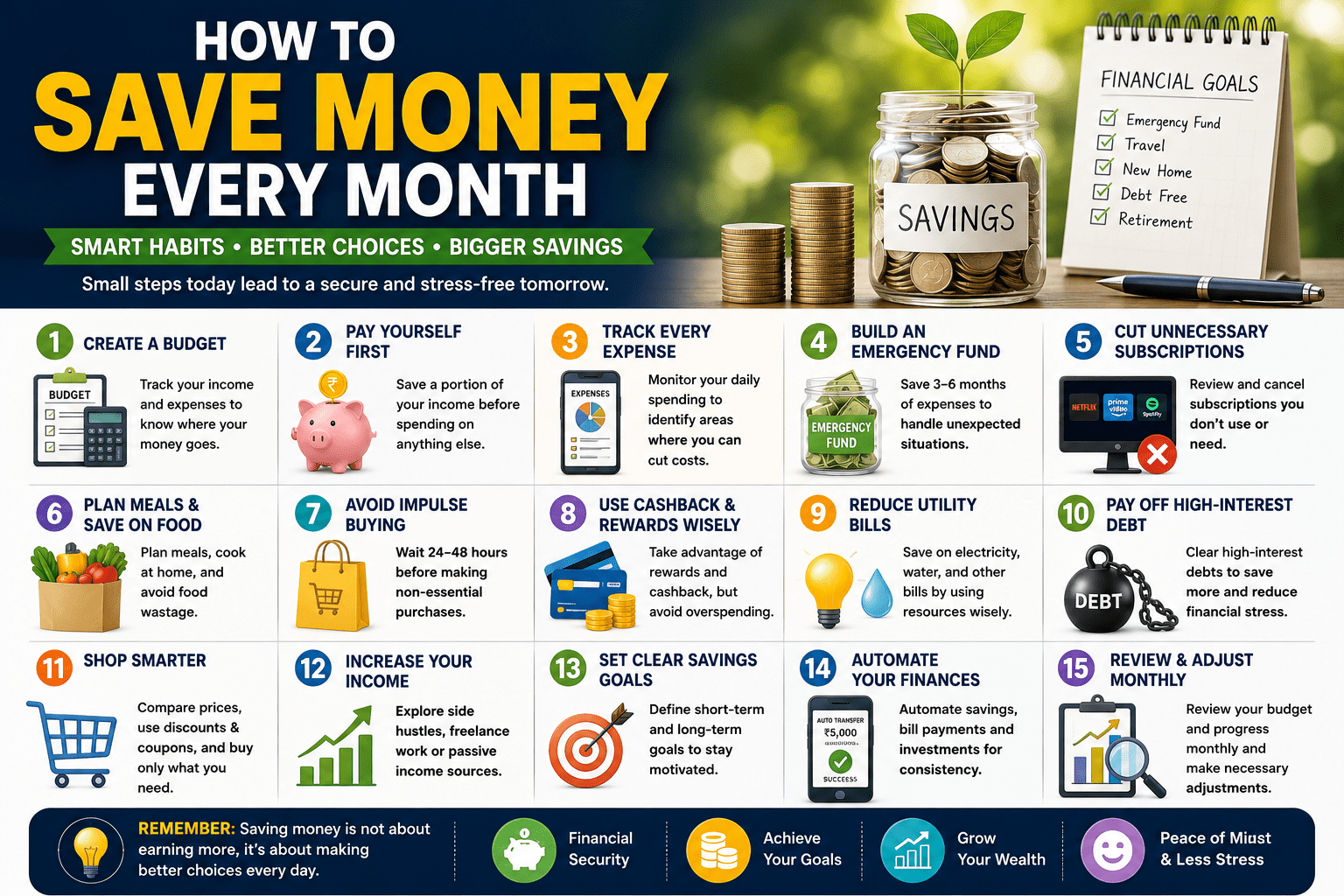

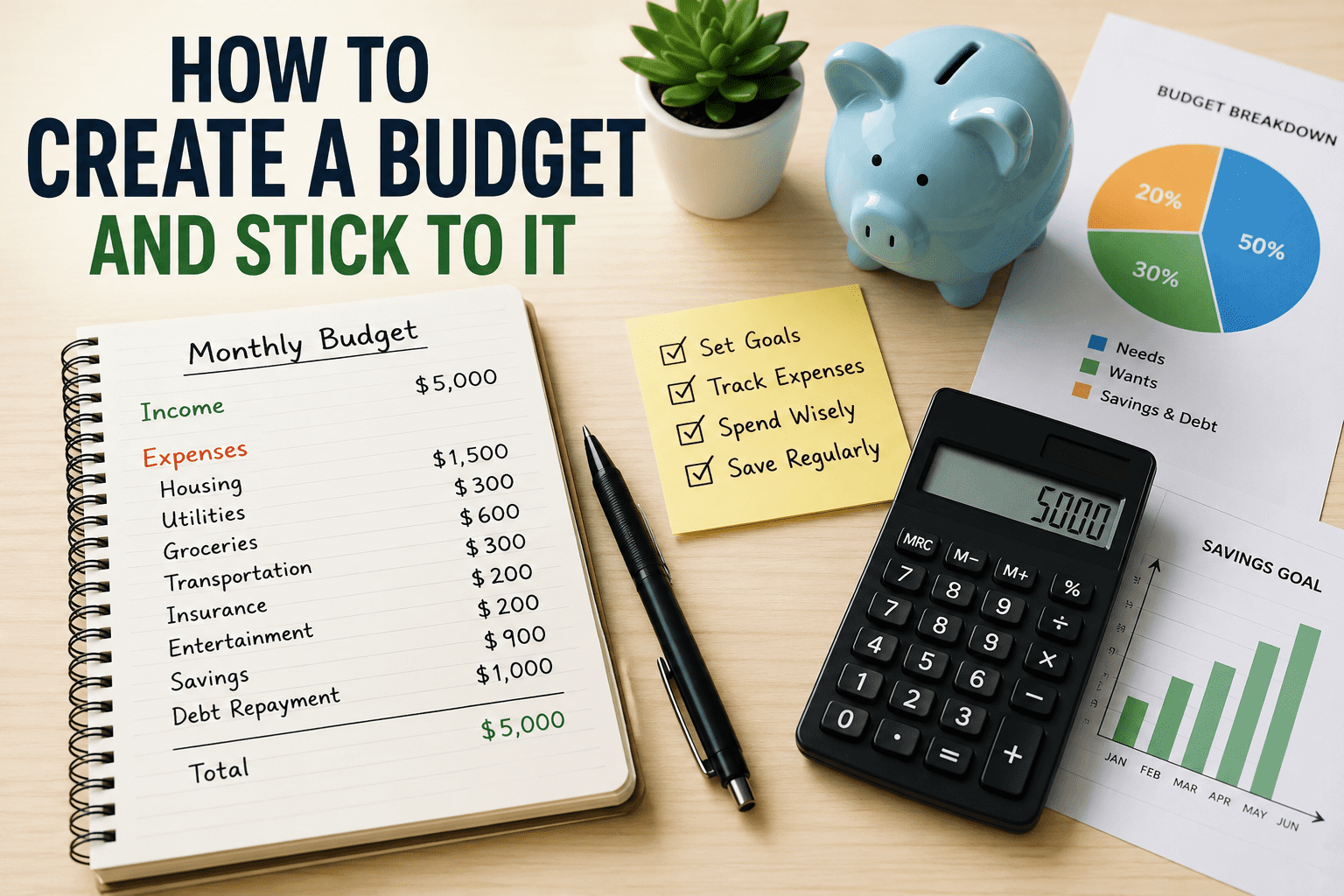

1. Create a Monthly Budget

The first step toward saving money is understanding where your money goes.

A monthly budget helps you:

- Track income and expenses

- Identify unnecessary spending

- Set savings goals

- Stay financially organized

Popular Budgeting Methods:

50/30/20 Rule

- 50% for necessities

- 30% for wants

- 20% for savings and investments

Zero-Based Budgeting

Assign every rupee or dollar a specific purpose before the month begins.

Budgeting creates awareness and prevents overspending.

2. Pay Yourself First

One of the most effective saving strategies is to save before spending.

Set up automatic transfers to:

- Savings accounts

- Investment accounts

- Retirement funds

- Emergency funds

Treat savings like a mandatory monthly expense.

Example:

If you earn ₹50,000 monthly, automatically transfer ₹5,000–₹10,000 to savings as soon as your salary arrives.

3. Track Every Expense

Small purchases often add up quickly.

Track spending on:

- Food delivery

- Coffee

- Online subscriptions

- Entertainment

- Impulse purchases

Expense tracking helps identify spending patterns and areas where you can cut costs.

4. Build an Emergency Fund

Unexpected expenses can derail your finances.

An emergency fund helps cover:

- Medical emergencies

- Car repairs

- Home maintenance

- Job loss

- Family emergencies

Financial experts recommend saving three to six months’ worth of living expenses.

5. Reduce Unnecessary Subscriptions

Many people pay for services they rarely use.

Review recurring expenses such as:

- Streaming platforms

- Mobile apps

- Gym memberships

- Software subscriptions

- Premium memberships

Cancel services that no longer provide value.

6. Plan Meals and Reduce Food Costs

Food expenses are often one of the largest monthly spending categories.

Ways to save include:

- Meal planning

- Cooking at home

- Buying groceries in bulk

- Reducing food waste

- Using discounts and coupons

Preparing meals at home can significantly lower monthly expenses.

7. Avoid Impulse Buying

Impulse purchases can quickly drain your budget.

Before making non-essential purchases:

- Wait 24 to 48 hours

- Compare prices

- Evaluate actual need

- Check reviews

This simple habit often prevents unnecessary spending.

8. Use Cashback and Reward Programs

Take advantage of:

- Cashback credit cards

- Shopping rewards

- Loyalty programs

- Discount offers

When used responsibly, these programs can help reduce overall expenses.

Important Tip:

Never overspend just to earn rewards.

9. Reduce Utility Bills

Lowering household expenses can create substantial monthly savings.

Consider:

- Using energy-efficient appliances

- Turning off unused electronics

- Conserving water

- Switching to LED lighting

- Monitoring electricity usage

Small changes can lead to significant savings over time.

10. Pay Off High-Interest Debt

Debt payments can consume a large portion of your income.

Focus on paying off:

- Credit card balances

- Personal loans

- High-interest borrowing

Reducing debt lowers interest costs and frees up money for savings.

11. Shop Smarter

Become a strategic shopper by:

- Comparing prices online

- Waiting for sales

- Buying generic brands

- Using discount codes

- Purchasing only what you need

Smart shopping habits help maximize the value of every purchase.

12. Increase Your Income

While reducing expenses is important, increasing income can accelerate savings.

Consider:

- Freelancing

- Side businesses

- Online consulting

- Selling digital products

- Affiliate marketing

Additional income can be directed entirely toward savings and investments.

13. Set Clear Savings Goals

Specific goals make saving easier and more motivating.

Examples include:

- Emergency fund

- New vehicle

- Home down payment

- Vacation

- Education expenses

- Retirement planning

Clear targets help maintain financial discipline.

14. Automate Your Finances

Automation removes the temptation to spend money that should be saved.

Automate:

- Savings transfers

- Bill payments

- Investment contributions

- Loan payments

This strategy ensures consistency without requiring constant effort.

15. Review Your Finances Monthly

Financial situations change over time.

Monthly reviews help you:

- Monitor progress

- Adjust budgets

- Identify spending leaks

- Improve financial habits

Regular reviews keep you focused on your goals.

Common Money-Saving Mistakes

Avoid these common mistakes:

- Saving only when money is left over

- Ignoring small expenses

- Carrying high-interest debt

- Not having an emergency fund

- Making emotional purchases

- Failing to track spending

Recognizing these pitfalls can help improve your financial results.

Benefits of Consistent Saving

Saving money every month provides numerous benefits:

- Greater financial security

- Reduced stress

- Increased investment opportunities

- Better emergency preparedness

- Faster achievement of financial goals

- Long-term wealth creation

The earlier you begin saving, the more powerful compound growth becomes.

Conclusion

Learning how to save money every month is one of the most valuable financial skills you can develop. By creating a budget, tracking expenses, reducing unnecessary spending, automating savings, and setting clear goals, you can steadily build financial security and achieve long-term success.

Remember that saving money is not about deprivation—it’s about making intentional financial decisions that align with your goals. Even small monthly contributions can grow into substantial savings over time. Start today, stay consistent, and watch your financial future become stronger month after month.

Also read Best Passive Income Ideas for 2026

Leave a Reply