Your 20s are one of the most important decades for building a strong financial foundation. The decisions you make during these years can significantly impact your future wealth, financial security, and overall quality of life. While it’s natural to make mistakes while learning about money, some financial errors can have long-lasting consequences.

The good news is that understanding these common money mistakes can help you avoid them and set yourself up for long-term success. Whether you’re starting your first job, paying off student loans, or planning your future, avoiding these financial pitfalls can make a huge difference.

Let’s explore the biggest money mistakes people make in their 20s and how you can avoid them.

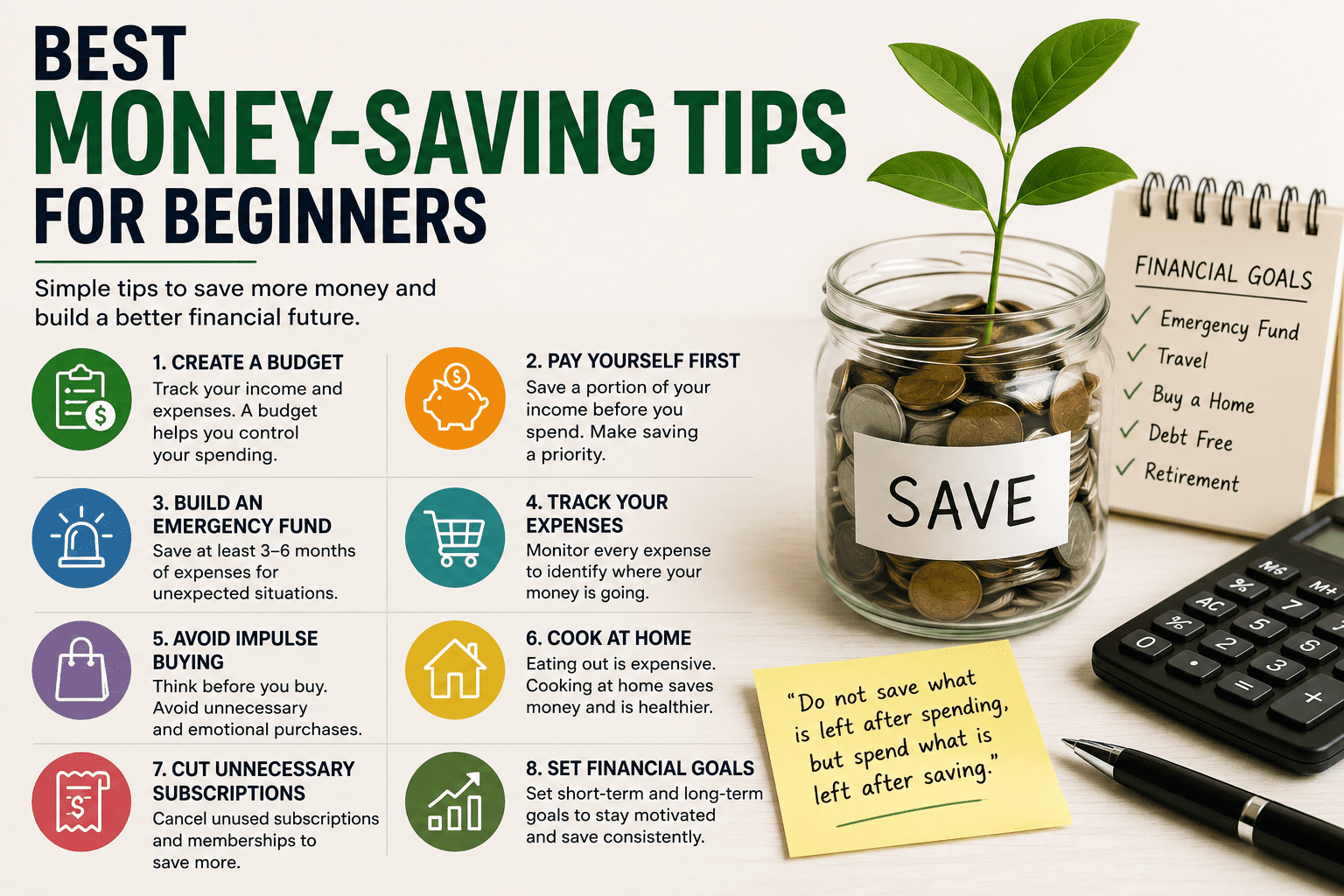

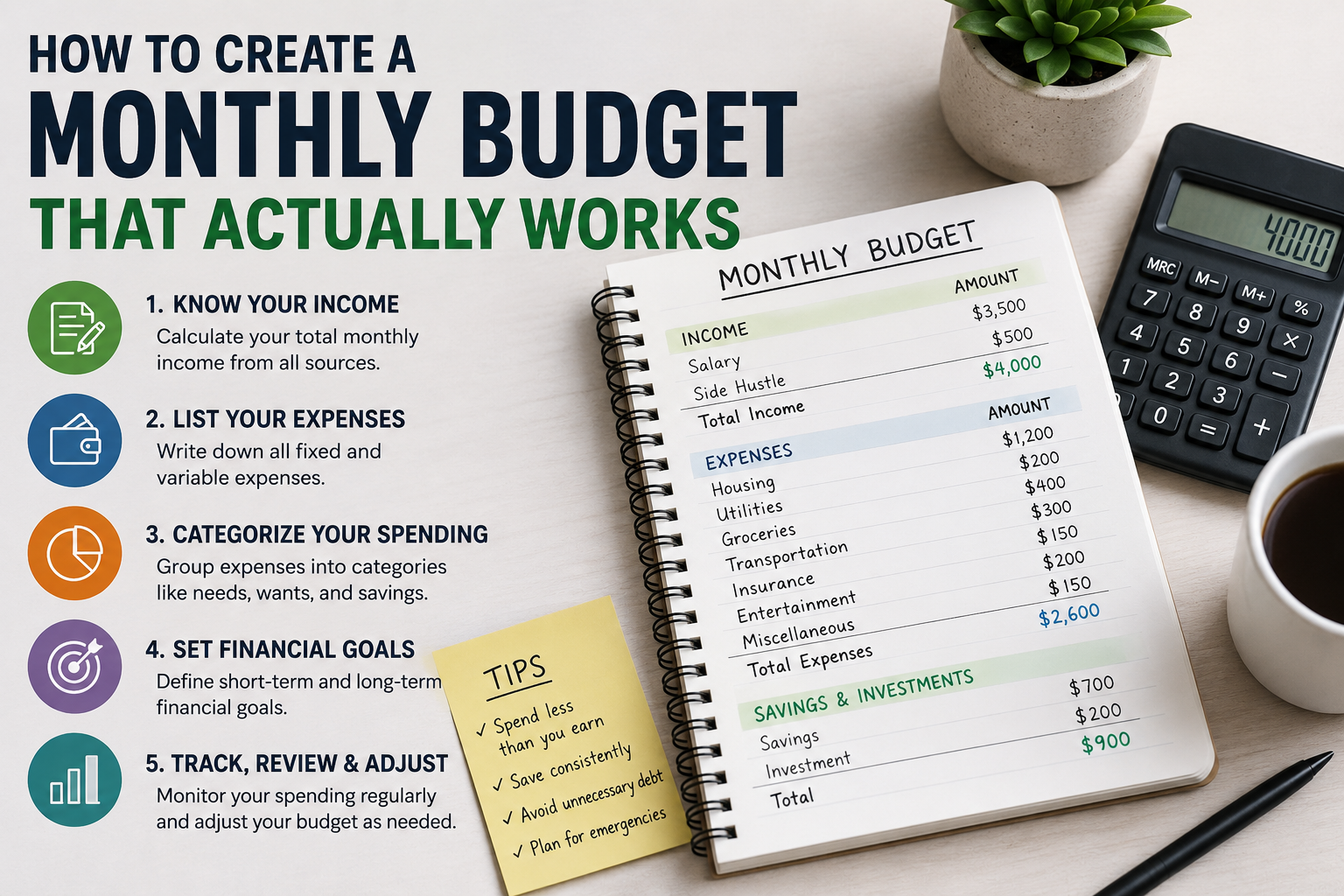

1. Not Creating a Budget

Many young adults assume budgeting is only necessary when money is tight. In reality, a budget is one of the most powerful financial tools regardless of income level.

Without a budget, it’s easy to:

- Overspend

- Accumulate debt

- Miss savings goals

- Lose track of expenses

How to Avoid This Mistake

Create a monthly budget that includes:

- Housing expenses

- Transportation costs

- Food and groceries

- Entertainment

- Savings and investments

A simple budget helps you stay in control of your finances.

2. Living Beyond Your Means

One of the most common financial mistakes in your 20s is spending more than you earn. Social media often creates pressure to maintain a lifestyle that may not align with your income.

Common examples include:

- Expensive vacations

- Luxury gadgets

- Designer clothing

- Frequent dining out

Smart Alternative

Focus on living below your means and saving the difference. Building wealth is easier when your expenses remain lower than your income.

3. Ignoring Emergency Savings

Unexpected expenses can happen at any time. Medical bills, car repairs, or sudden job loss can quickly create financial stress.

Many young adults make the mistake of relying on credit cards when emergencies arise.

Solution

Build an emergency fund that covers:

- Three to six months of living expenses

- Essential bills and necessities

An emergency fund provides financial security and peace of mind.

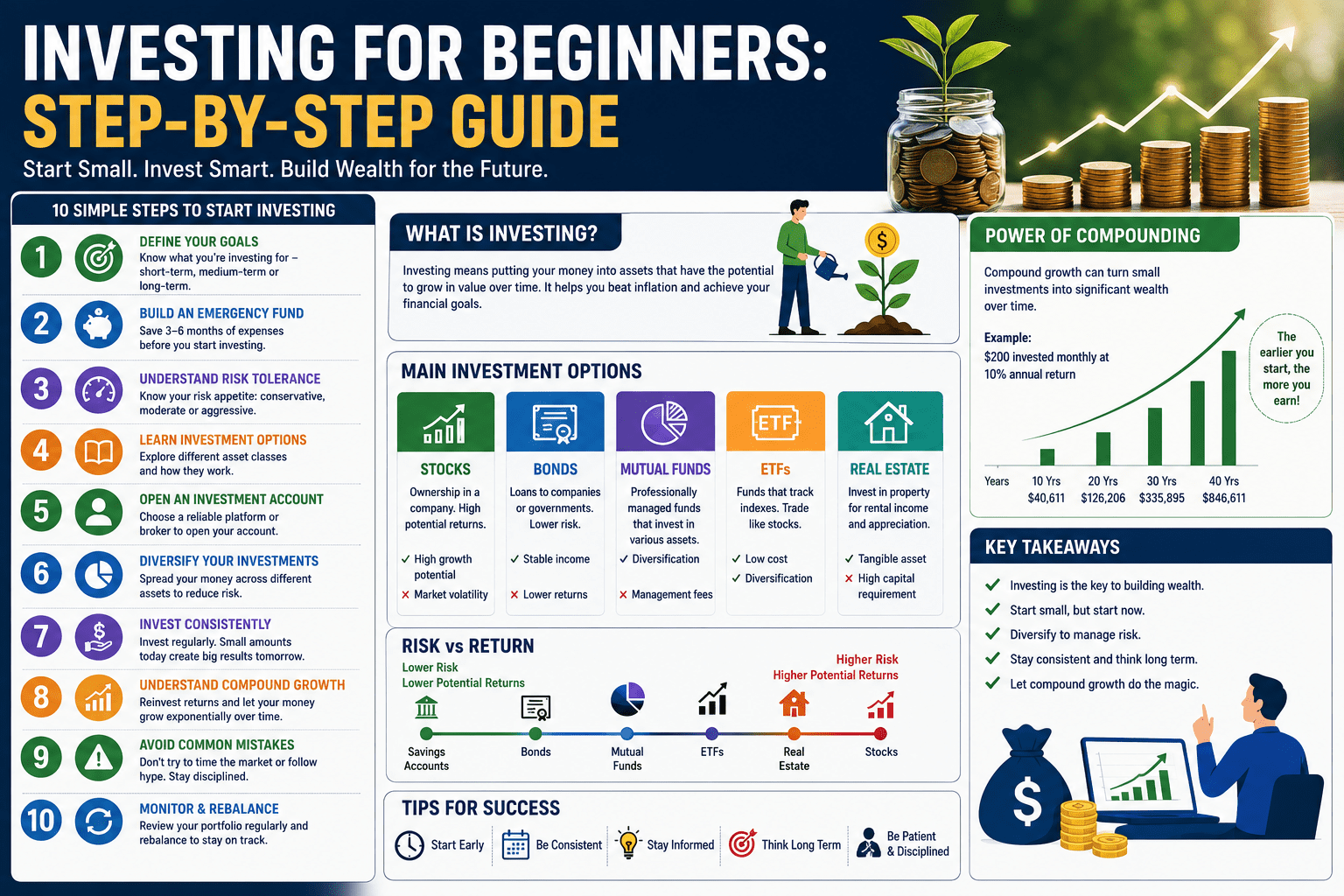

4. Delaying Investing

Many people believe investing is only for older individuals or high-income earners. This misconception often leads to missed opportunities.

The biggest advantage young investors have is time.

Why Starting Early Matters

Even small investments made in your 20s can grow significantly through compound returns over several decades.

Benefits include:

- Long-term wealth growth

- Financial independence

- Retirement security

The earlier you start investing, the more time your money has to grow.

5. Accumulating Credit Card Debt

Credit cards can be useful financial tools when used responsibly. However, carrying balances and paying high interest rates can become a major obstacle to financial success.

Common Credit Card Mistakes

- Paying only the minimum balance

- Impulse purchases

- Using credit for everyday expenses

- Missing payment deadlines

Better Approach

Pay your balance in full each month whenever possible and use credit strategically.

6. Failing to Set Financial Goals

Without clear goals, it’s easy to spend money without purpose.

Examples of financial goals include:

- Buying a home

- Starting a business

- Paying off debt

- Building an investment portfolio

- Achieving financial freedom

Goals provide direction and motivation for making smarter financial choices.

7. Not Learning About Personal Finance

Schools often teach mathematics and science but rarely cover personal finance in depth. As a result, many young adults enter the workforce without understanding how money works.

Topics worth learning include:

- Budgeting

- Investing

- Taxes

- Insurance

- Retirement planning

Financial education can save thousands of dollars in future mistakes.

8. Lifestyle Inflation

When income increases, many people immediately increase their spending. This phenomenon is known as lifestyle inflation.

Examples include:

- Upgrading apartments

- Purchasing expensive vehicles

- Increasing discretionary spending

Why It’s Dangerous

If spending rises as quickly as income, wealth accumulation becomes difficult.

Instead:

- Save part of every raise

- Increase investments

- Maintain reasonable living expenses

9. Neglecting Retirement Planning

Retirement may seem decades away in your 20s, but delaying retirement savings is one of the costliest mistakes people make.

Starting early allows compound growth to work in your favor.

Retirement Planning Tips

- Contribute regularly to retirement accounts.

- Increase contributions over time.

- Take advantage of employer matching programs if available.

Small contributions today can become substantial wealth in the future.

10. Relying on One Source of Income

Many young professionals depend entirely on their primary job for income.

While a stable job is valuable, relying on a single income source can be risky.

Consider Building Additional Income Streams

- Freelancing

- Blogging

- Affiliate marketing

- Dividend investing

- Online businesses

- Digital products

Multiple income streams can improve financial security and accelerate wealth creation.

11. Ignoring Insurance Coverage

Many people in their 20s underestimate the importance of insurance.

Insurance helps protect against unexpected financial losses.

Important types include:

- Health insurance

- Vehicle insurance

- Life insurance (when appropriate)

- Disability coverage

Adequate protection can prevent financial disasters.

12. Trying to Keep Up With Others

Comparing yourself to friends, coworkers, or social media influencers often leads to poor financial decisions.

Common consequences include:

- Overspending

- Excessive debt

- Delayed savings goals

Remember that financial success is a personal journey, not a competition.

The Long-Term Impact of Financial Mistakes

The consequences of financial mistakes in your 20s often extend far beyond the decade itself.

Potential outcomes include:

- Lower retirement savings

- Increased debt burdens

- Delayed home ownership

- Reduced investment growth

- Greater financial stress

Fortunately, recognizing these mistakes early allows you to correct course and improve your future.

Smart Financial Habits to Build in Your 20s

To strengthen your financial future:

Start Saving Consistently

Save a portion of every paycheck.

Invest Early

Take advantage of long-term growth opportunities.

Track Spending

Know where your money goes each month.

Continue Learning

Read books, listen to podcasts, and improve financial literacy.

Set Clear Goals

Give your money a purpose.

These habits create a strong foundation for future financial success.

Conclusion

Your 20s are a critical time for building lifelong financial habits. While making mistakes is part of learning, avoiding the most common money errors can significantly improve your financial future.

By creating a budget, avoiding unnecessary debt, investing early, building an emergency fund, and continuously educating yourself, you can develop financial habits that lead to long-term wealth and security.

The choices you make today will shape your financial future for decades to come. Start making smart money decisions now, and your future self will thank you.

Also read 10 Smart Money Habits That Can Change Your Financial Future

Leave a Reply