A good credit score is one of the most valuable financial assets you can have. It affects your ability to secure loans, qualify for credit cards, obtain favorable interest rates, and even rent a home. Whether you’re planning to apply for a mortgage, car loan, or personal credit card, improving your credit score can save you thousands of dollars over time.

The good news is that while building excellent credit takes time, there are several strategies you can use to improve your credit score quickly. In this guide, we’ll explore the most effective ways to boost your credit rating and strengthen your financial future.

What Is a Credit Score?

A credit score is a numerical representation of your creditworthiness. It helps lenders evaluate the risk of lending money to you.

Credit scores are typically based on factors such as:

- Payment history

- Credit utilization

- Length of credit history

- Types of credit accounts

- Recent credit inquiries

Higher scores indicate lower risk, making it easier to qualify for loans and favorable interest rates.

Why Your Credit Score Matters

A strong credit score can provide numerous benefits:

- Lower interest rates on loans

- Higher chances of loan approval

- Better credit card offers

- Increased borrowing limits

- Easier approval for rental housing

- Improved financial opportunities

Even a modest improvement in your credit score can have a significant impact on your financial life.

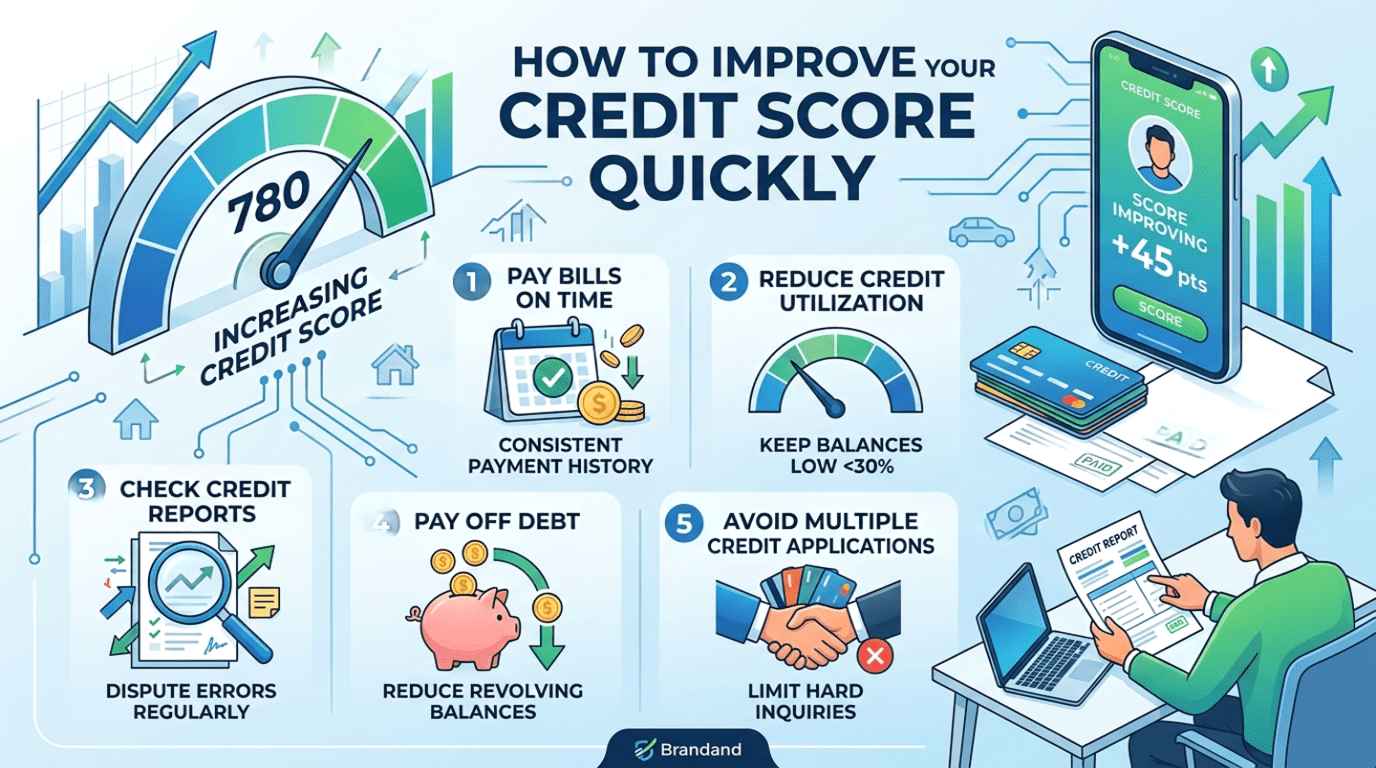

1. Pay Your Bills on Time

Payment history is one of the most important factors affecting your credit score.

How to Improve

- Pay all bills before the due date.

- Set up automatic payments.

- Use reminders and calendar alerts.

- Prioritize overdue accounts.

Consistently making on-time payments demonstrates financial responsibility and can improve your score over time.

2. Reduce Your Credit Utilization Ratio

Credit utilization refers to the percentage of available credit you’re currently using.

Example

If your credit card limit is ₹100,000 and your balance is ₹30,000, your utilization ratio is 30%.

Experts recommend keeping utilization below 30%, and ideally below 10%.

Ways to Lower Utilization

- Pay down existing balances.

- Make multiple payments each month.

- Request a credit limit increase.

- Avoid unnecessary spending.

Lower utilization can result in a relatively quick credit score improvement.

3. Check Your Credit Report for Errors

Credit report mistakes are more common than many people realize.

Errors may include:

- Incorrect account balances

- Duplicate accounts

- Fraudulent accounts

- Incorrect payment records

What to Do

- Obtain your credit report.

- Review it carefully.

- Dispute inaccurate information promptly.

Correcting errors can sometimes lead to a noticeable increase in your credit score.

4. Pay Off Outstanding Debt

Reducing debt is one of the fastest ways to improve your credit profile.

Prioritize High-Interest Debt

Focus on:

- Credit card balances

- Personal loans

- High-interest consumer debt

The lower your debt burden, the more attractive you appear to lenders.

5. Avoid Applying for Multiple Credit Accounts

Each credit application can result in a hard inquiry on your credit report.

Multiple inquiries within a short period may:

- Lower your credit score temporarily

- Signal financial distress to lenders

Apply for new credit only when necessary.

6. Become an Authorized User

If a trusted family member has a credit card with a strong payment history, becoming an authorized user may help improve your credit profile.

Benefits include:

- Access to positive payment history

- Improved credit utilization

- Faster credit-building opportunities

Ensure the primary account holder manages credit responsibly.

7. Keep Older Credit Accounts Open

The length of your credit history influences your credit score.

Closing older accounts can:

- Shorten your credit history

- Increase your utilization ratio

Unless there are significant fees, keeping older accounts open often benefits your score.

8. Diversify Your Credit Mix

Lenders like to see responsible management of different types of credit.

Examples include:

- Credit cards

- Auto loans

- Personal loans

- Mortgages

A healthy mix of credit accounts can positively impact your score over time.

9. Negotiate with Creditors

If you have missed payments or collections accounts, contact creditors directly.

Possible solutions include:

- Payment plans

- Settlement agreements

- Goodwill adjustments

Some creditors may update your account status after resolving outstanding balances.

10. Use Credit Responsibly Going Forward

Long-term credit improvement requires consistent financial habits.

Best Practices

- Pay balances in full whenever possible.

- Avoid maxing out credit cards.

- Monitor your credit regularly.

- Stick to a realistic budget.

- Maintain emergency savings.

Responsible financial behavior supports sustainable credit growth.

Common Mistakes That Hurt Credit Scores

Avoid these costly errors:

Missing Payments

Late payments can significantly damage your credit profile.

Maxing Out Credit Cards

High utilization signals financial stress.

Closing Old Accounts

This can reduce your average credit age.

Applying for Too Much Credit

Frequent applications can lower your score.

Ignoring Credit Reports

Unnoticed errors may continue affecting your credit.

How Long Does It Take to Improve a Credit Score?

The timeline depends on your financial situation.

Potential Improvements

- Credit utilization reductions may impact scores within weeks.

- Error corrections can improve scores within one to three months.

- Consistent on-time payments typically show results within several months.

- Significant credit rebuilding may take one to two years.

Patience and consistency are key to achieving lasting improvements.

Benefits of a Higher Credit Score

Improving your credit score can lead to:

- Lower borrowing costs

- Better loan approvals

- Higher credit limits

- Increased financial flexibility

- Better insurance rates in some regions

- Greater confidence in financial planning

These advantages can help you save money and achieve your financial goals faster.

Conclusion

Improving your credit score quickly requires a combination of smart financial decisions and consistent habits. Paying bills on time, reducing credit card balances, checking for errors, avoiding unnecessary credit applications, and managing debt responsibly are among the most effective strategies.

While some improvements can happen within weeks, building excellent credit is a long-term process. By following these proven techniques, you can strengthen your credit profile, improve your financial health, and unlock better opportunities for loans, credit cards, and future investments.

Also read How to Save Money Every Month

Leave a Reply