Starting a career is an exciting milestone. Along with new opportunities and increased income comes the responsibility of managing finances wisely. Financial planning is essential for young professionals who want to achieve financial security, reduce stress, and build wealth for the future.

Many young adults focus on earning money but overlook the importance of creating a financial strategy. Without a proper plan, it becomes easy to accumulate debt, overspend, or miss valuable investment opportunities. The good news is that developing healthy financial habits early can have a significant impact on long-term financial success.

In this guide, we’ll explore practical financial planning strategies that can help young professionals take control of their money and achieve their financial goals.

What Is Financial Planning?

Financial planning is the process of managing your income, expenses, savings, investments, and financial goals to achieve long-term stability and growth.

A good financial plan helps you:

- Manage money effectively

- Build emergency savings

- Reduce debt

- Grow wealth through investments

- Prepare for retirement

- Achieve personal and professional goals

Financial planning is not only for wealthy individuals. Everyone can benefit from having a structured financial roadmap.

Why Financial Planning Is Important for Young Professionals

Many young professionals are just beginning their financial journey. This stage offers a unique advantage: time.

Starting early allows you to:

- Benefit from compound interest

- Develop disciplined spending habits

- Build a strong credit history

- Avoid unnecessary debt

- Create long-term financial security

The earlier you begin planning, the easier it becomes to achieve major life goals such as buying a home, starting a business, or retiring comfortably.

Assess Your Current Financial Situation

Before creating a financial plan, evaluate your current financial health.

Review:

- Monthly income

- Living expenses

- Existing debt

- Savings accounts

- Investment accounts

- Financial obligations

Understanding your financial position helps identify areas that need improvement.

Calculate Your Net Worth

Net worth equals:

Assets – Liabilities = Net Worth

Assets include:

- Savings

- Investments

- Property

- Valuable possessions

Liabilities include:

- Student loans

- Credit card debt

- Personal loans

- Other obligations

Tracking net worth helps measure financial progress over time.

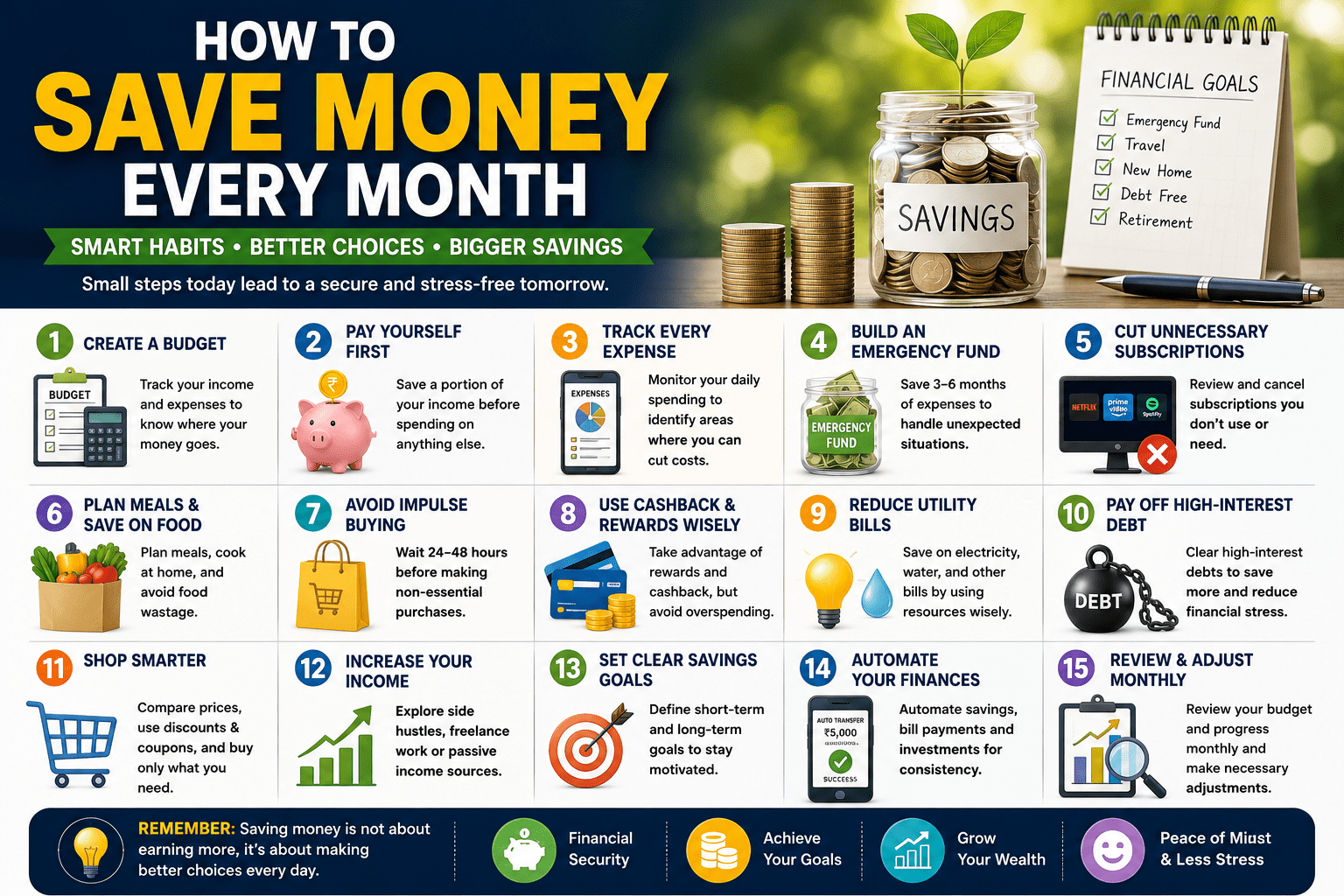

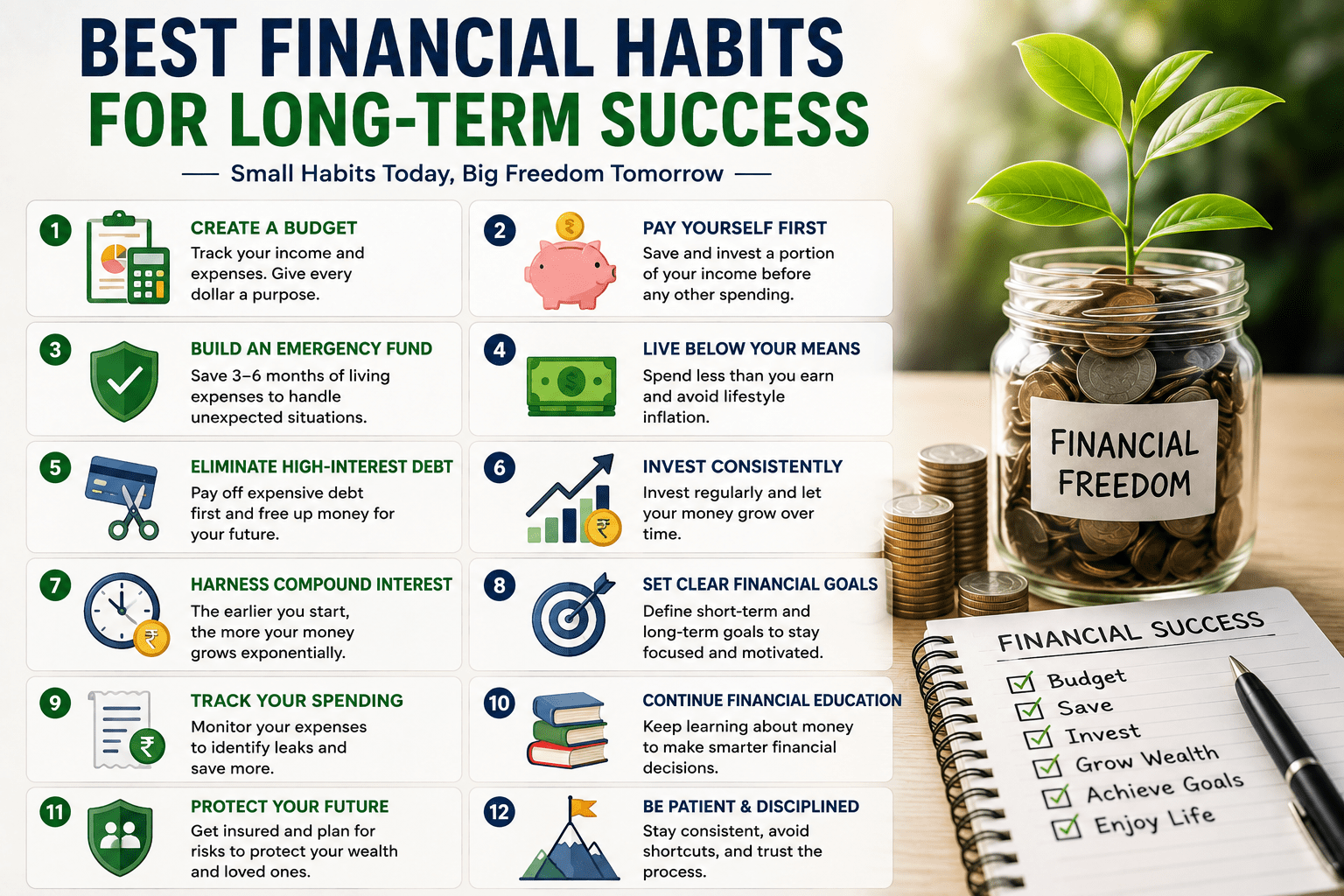

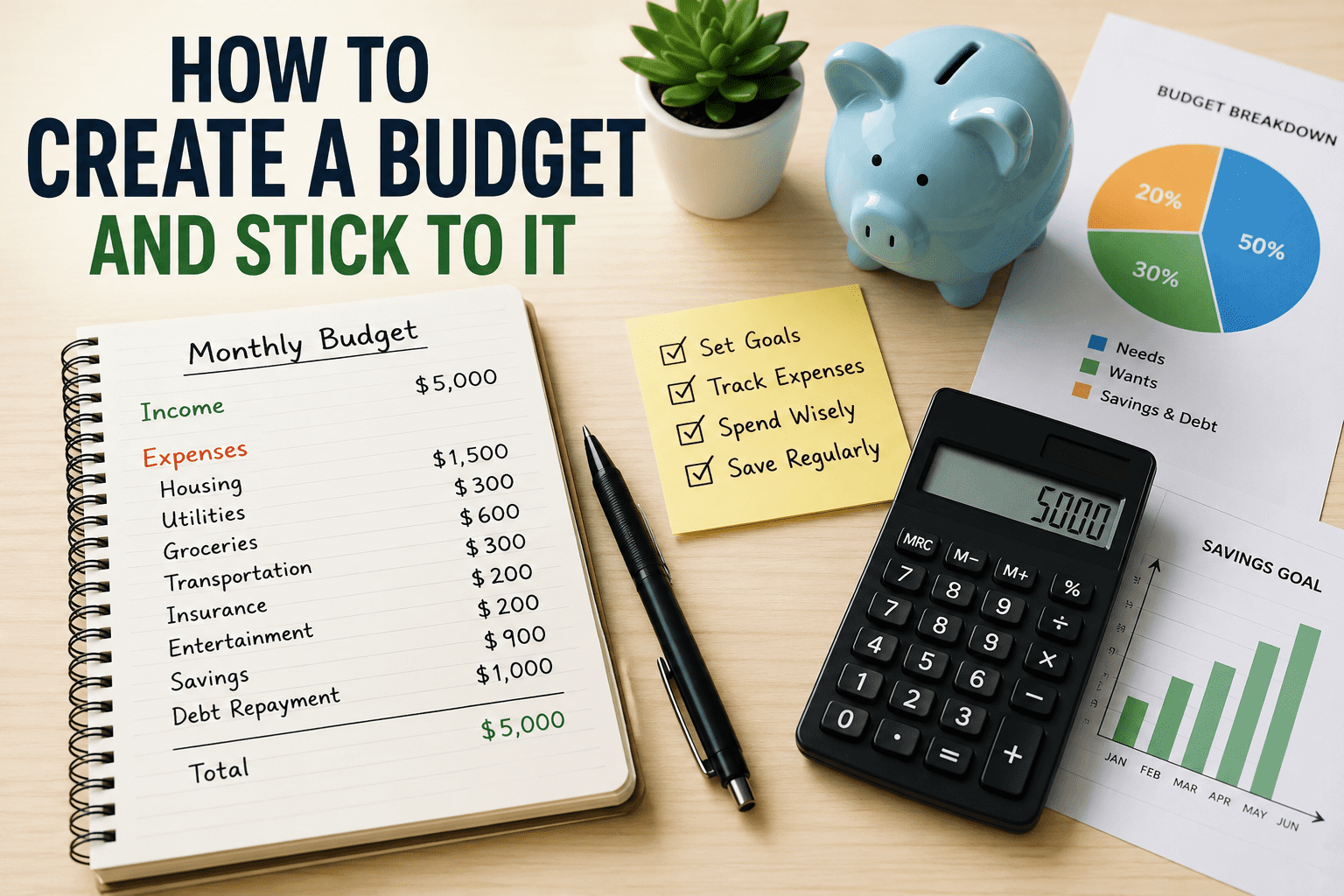

Create a Realistic Budget

A budget is the foundation of financial planning.

A simple budgeting method is the 50/30/20 Rule:

50% for Needs

Essential expenses such as:

- Rent

- Utilities

- Transportation

- Insurance

- Groceries

30% for Wants

Lifestyle expenses including:

- Entertainment

- Dining out

- Travel

- Shopping

20% for Savings and Investments

Allocate this portion toward:

- Emergency funds

- Retirement savings

- Investments

- Debt repayment

Budgeting helps ensure your money aligns with your priorities.

Build an Emergency Fund

Unexpected expenses can arise at any time.

Examples include:

- Medical emergencies

- Car repairs

- Job loss

- Home maintenance

Financial experts generally recommend saving three to six months of living expenses in an easily accessible emergency fund.

Benefits include:

- Reduced financial stress

- Protection from debt

- Greater financial stability

Start small and contribute consistently.

Manage Debt Wisely

Debt can limit financial growth if not managed properly.

Common types of debt include:

- Student loans

- Credit card balances

- Personal loans

- Auto loans

Strategies for Debt Management

Pay High-Interest Debt First

Focus on paying off debts with the highest interest rates.

Avoid Unnecessary Borrowing

Only take on debt when necessary and manageable.

Make Payments on Time

Timely payments help improve your credit score and reduce interest costs.

Reducing debt frees up more money for savings and investments.

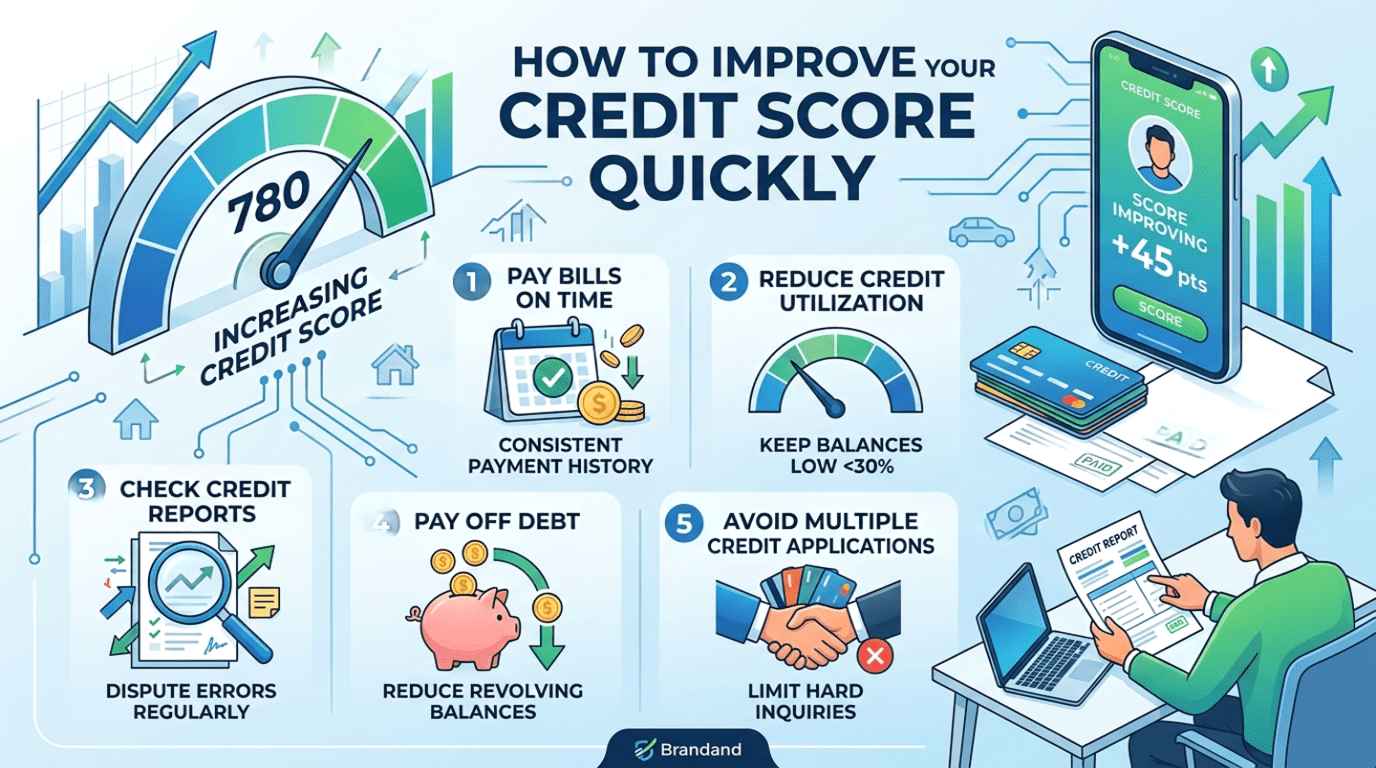

Understand the Importance of Credit Scores

Your credit score affects your ability to:

- Obtain loans

- Rent housing

- Secure favorable interest rates

- Access certain financial products

Tips to improve your credit score:

- Pay bills on time

- Keep credit utilization low

- Avoid excessive credit applications

- Maintain older credit accounts

A strong credit profile can save thousands of dollars over time.

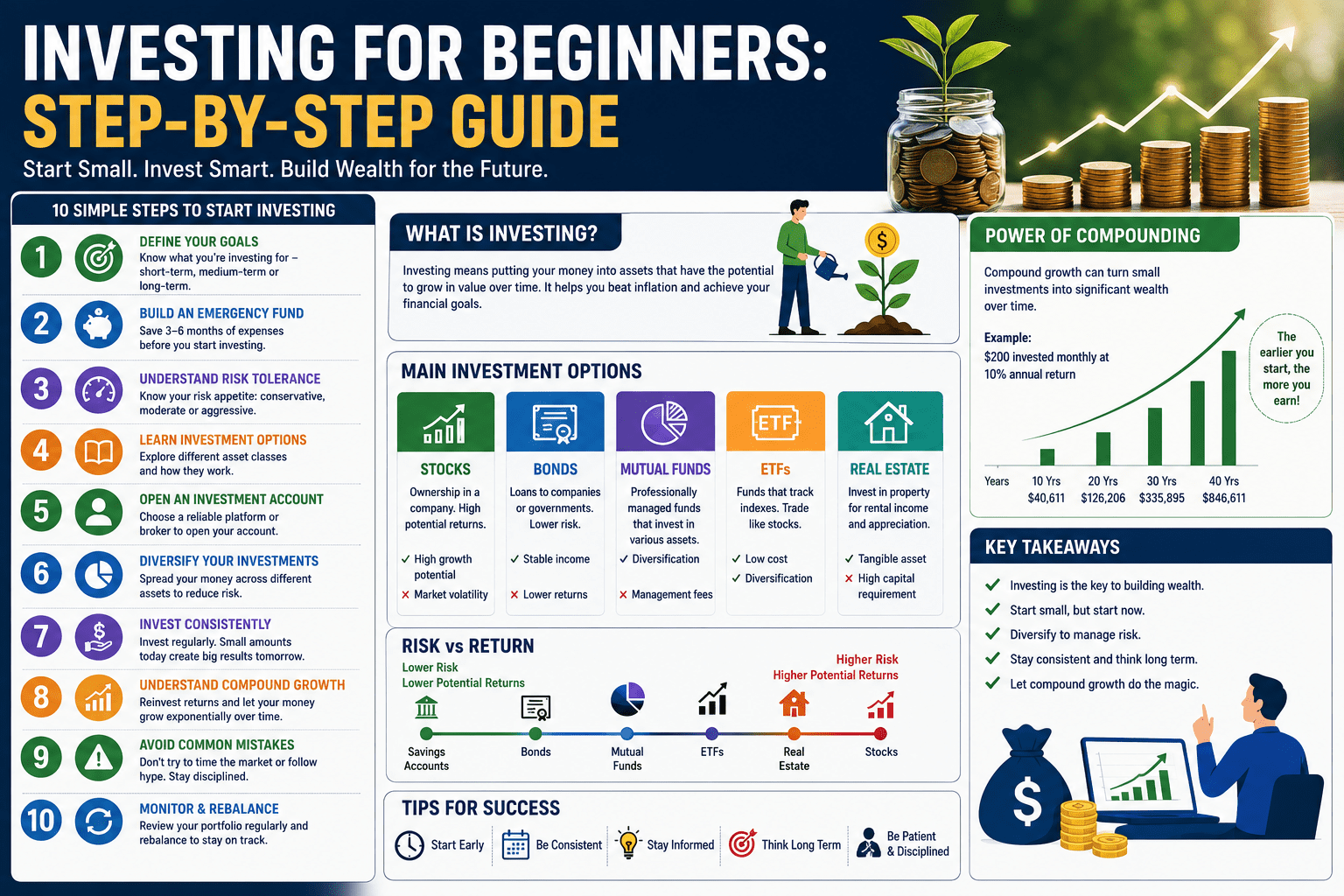

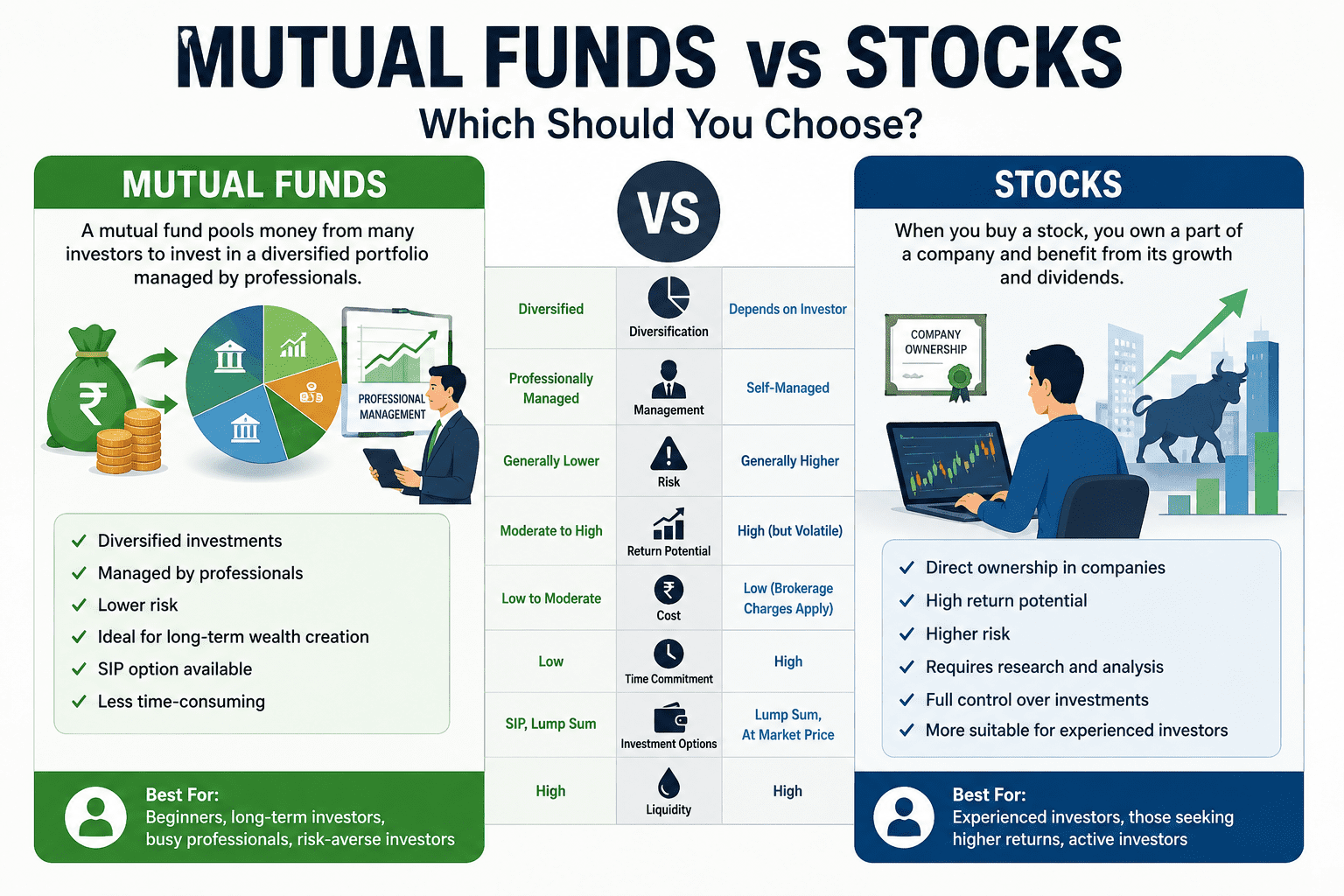

Start Investing Early

Investing is one of the most effective ways to build wealth.

The power of compound growth means your money can generate earnings that continue to grow over time.

Popular Investment Options

Stocks

Offer high growth potential but come with higher risk.

Mutual Funds

Provide diversification by pooling investments.

Index Funds

Track market indexes and typically have lower fees.

Exchange-Traded Funds (ETFs)

Offer flexibility and diversification.

Bonds

Generally provide lower risk and stable returns.

Investing early allows your money more time to grow.

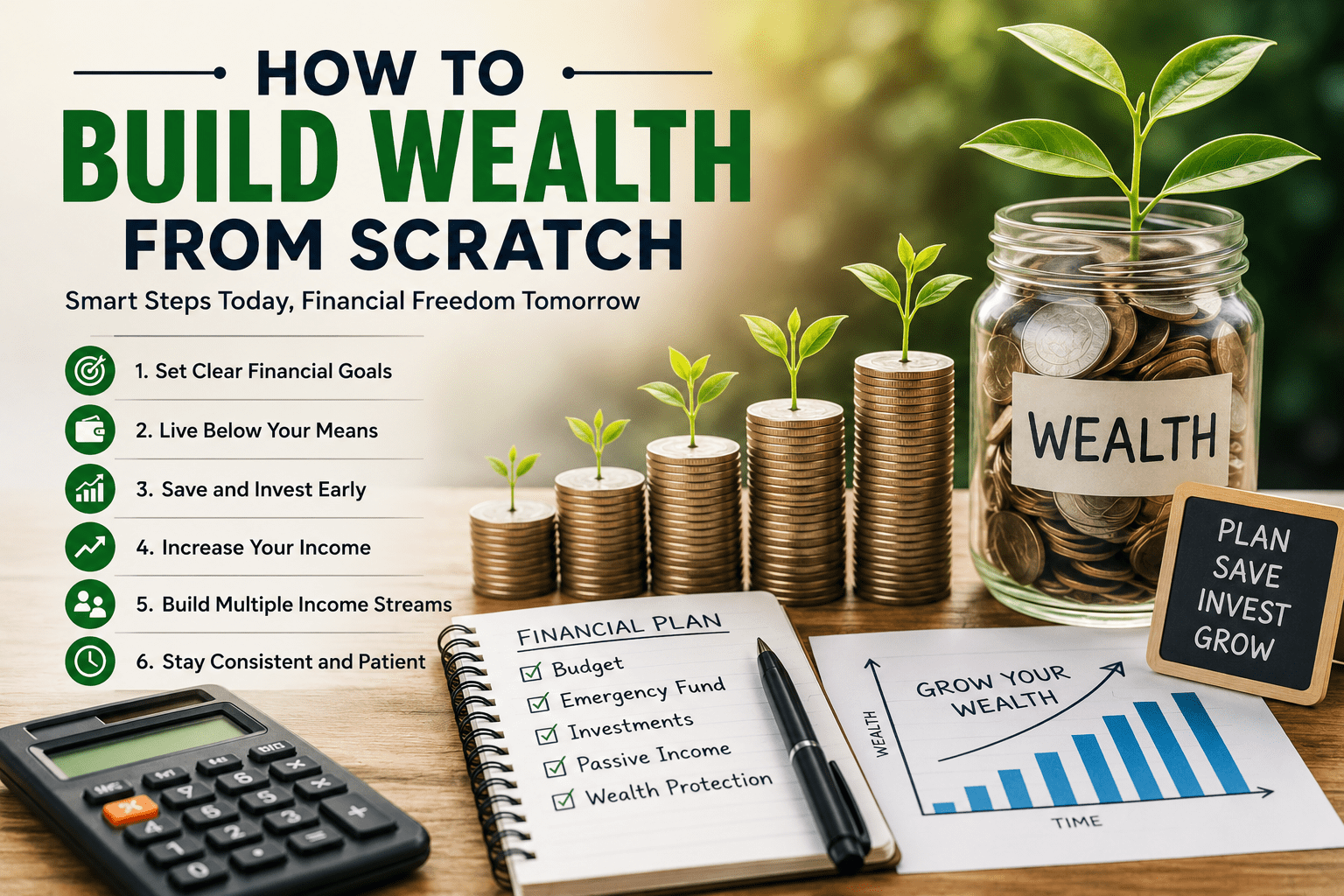

Set Financial Goals

Clear goals provide direction and motivation.

Short-Term Goals

Examples include:

- Building an emergency fund

- Paying off credit cards

- Saving for travel

Medium-Term Goals

Examples include:

- Purchasing a car

- Starting a business

- Saving for higher education

Long-Term Goals

Examples include:

- Homeownership

- Financial independence

- Retirement

SMART goals are:

- Specific

- Measurable

- Achievable

- Relevant

- Time-bound

Plan for Retirement Early

Retirement may seem far away, but starting early provides enormous advantages.

Benefits include:

- More time for investments to grow

- Reduced monthly contribution requirements

- Greater financial flexibility

Retirement planning options may include:

- Employer-sponsored retirement plans

- Pension schemes

- Individual retirement accounts

- Long-term investment portfolios

Even small contributions can grow significantly over decades.

Protect Yourself with Insurance

Insurance is an essential part of financial planning.

Important types include:

Health Insurance

Protects against medical expenses.

Life Insurance

Provides financial support to dependents.

Disability Insurance

Offers income protection if you’re unable to work.

Property Insurance

Protects valuable assets from unexpected losses.

Insurance helps safeguard your financial future.

Increase Your Income

Financial growth isn’t only about saving money.

Look for opportunities to increase earnings through:

- Skill development

- Certifications

- Freelancing

- Side businesses

- Career advancement

Investing in yourself often delivers the highest returns.

Avoid Common Financial Mistakes

Young professionals often make avoidable financial errors.

Lifestyle Inflation

Spending increases as income rises.

Ignoring Investments

Waiting too long to invest reduces growth potential.

Lack of Emergency Savings

Unexpected expenses can create financial hardship.

Excessive Credit Card Use

High-interest debt can quickly become overwhelming.

No Financial Goals

Without goals, financial decisions often lack direction.

Recognizing these mistakes early can prevent future financial challenges.

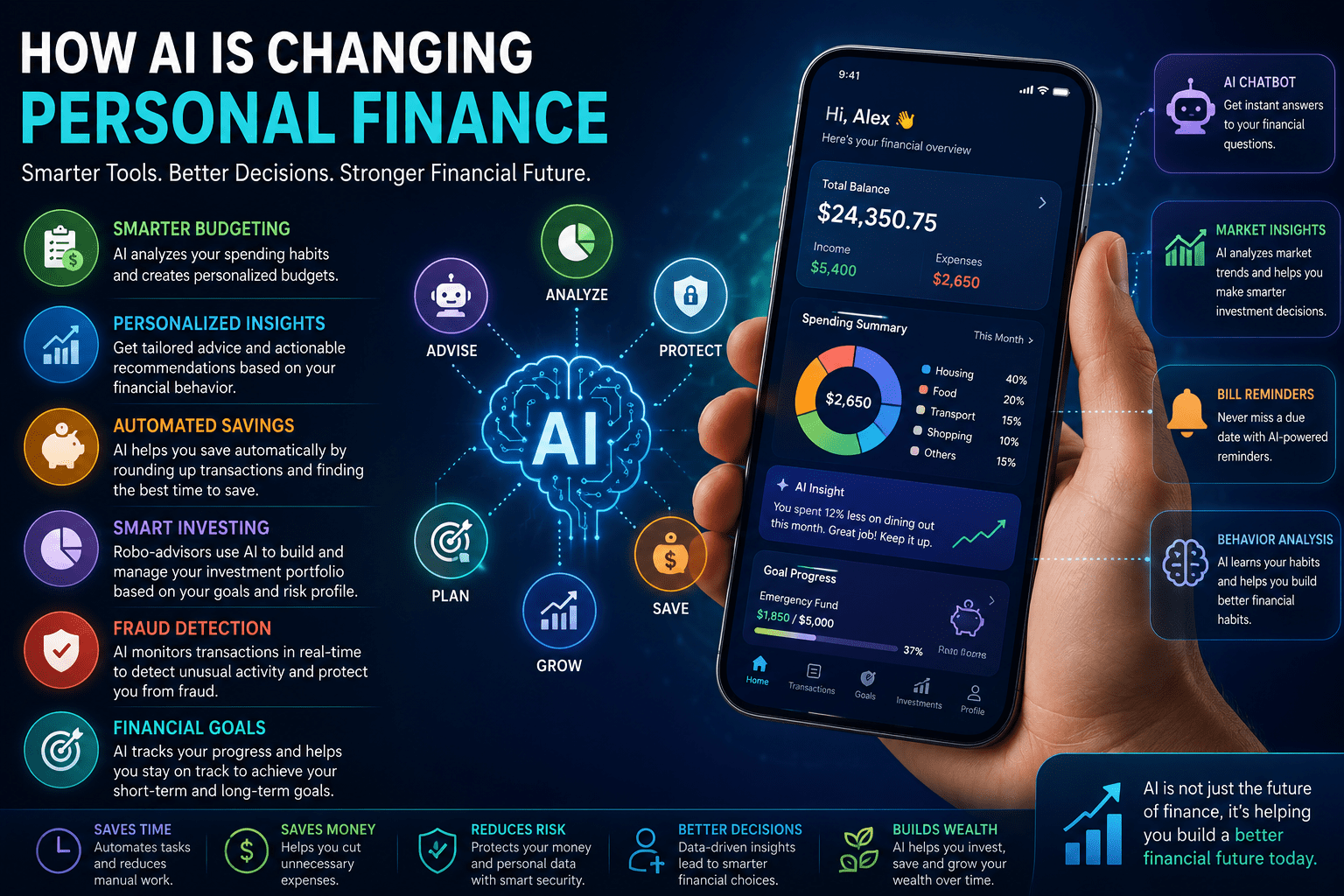

Technology and Personal Finance

Modern financial tools make money management easier than ever.

Useful tools include:

- Budgeting apps

- Investment platforms

- Expense trackers

- Retirement calculators

- Financial planning software

These tools help monitor progress and improve decision-making.

The Future of Financial Planning

Financial planning continues to evolve with technology.

Emerging trends include:

- AI-powered financial advisors

- Automated investing

- Digital banking

- Personalized financial insights

- Advanced budgeting tools

Young professionals who embrace financial technology can make smarter and more informed decisions.

Conclusion

Financial planning is one of the most valuable skills young professionals can develop. By creating a budget, building an emergency fund, managing debt, investing early, and setting clear goals, individuals can establish a strong foundation for long-term financial success.

The key is to start now. Small financial decisions made today can lead to significant rewards in the future. With discipline, consistency, and a clear plan, young professionals can achieve financial security, grow wealth, and confidently pursue their personal and professional aspirations.

Also read AI Tools for Personal Finance Management

Leave a Reply