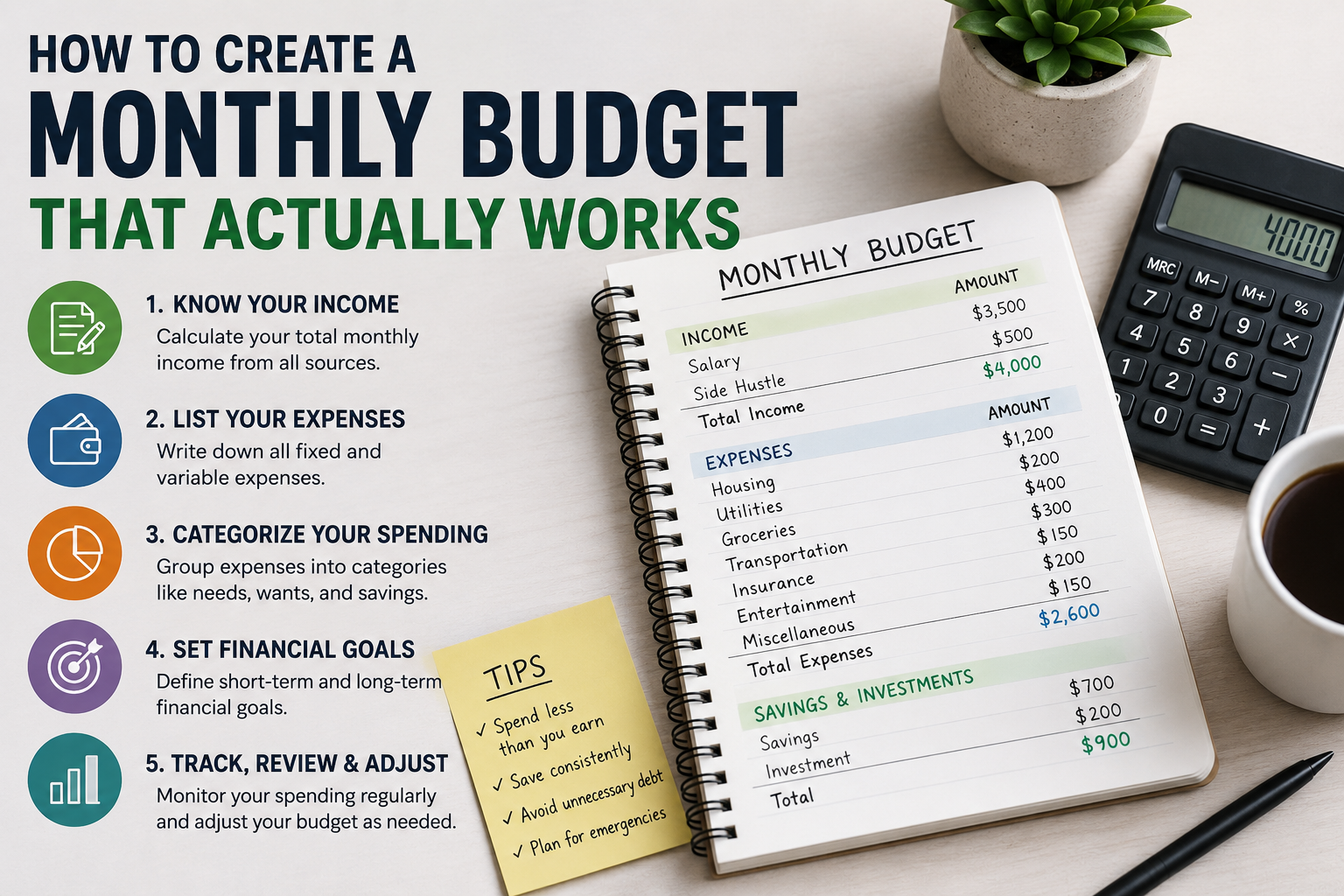

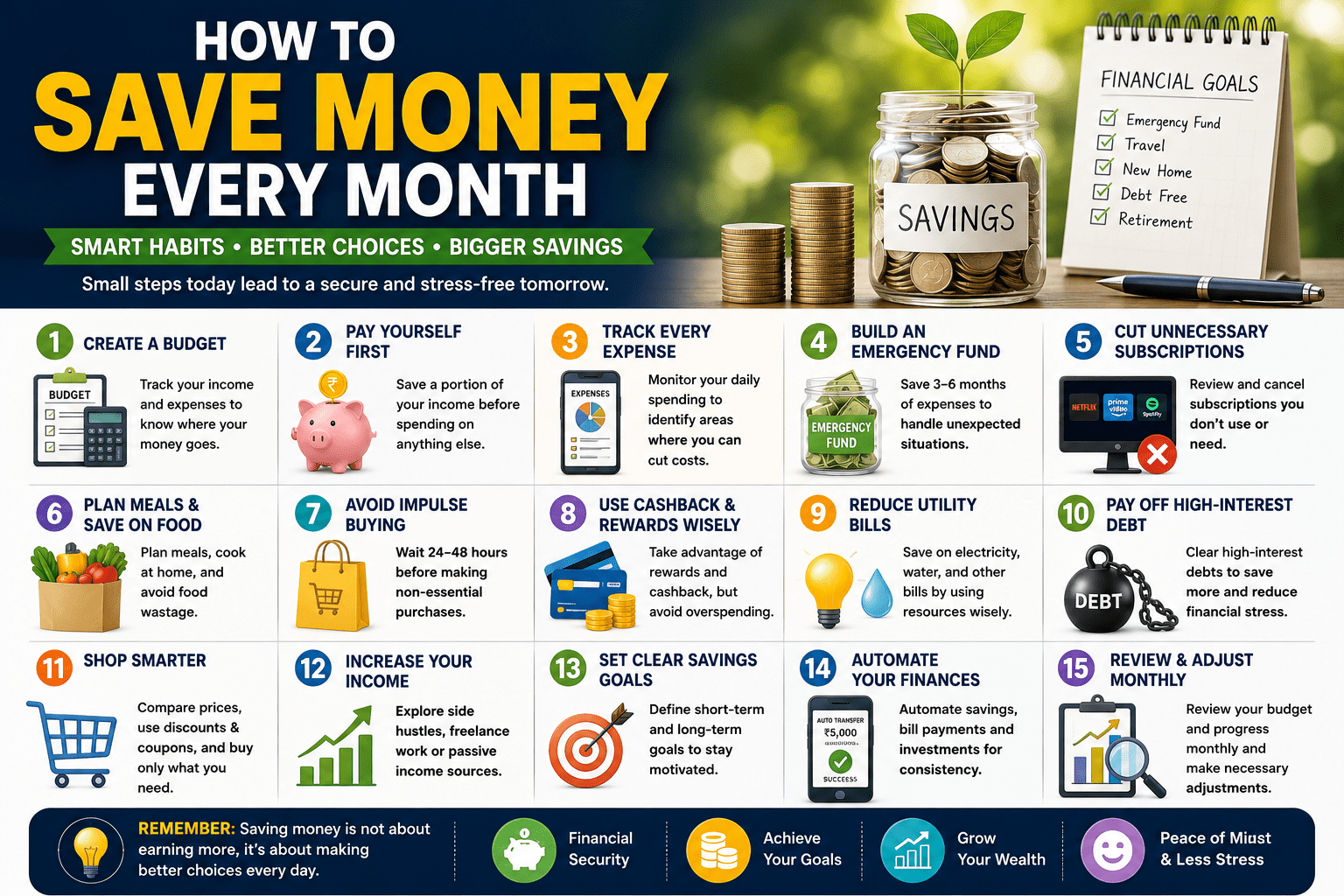

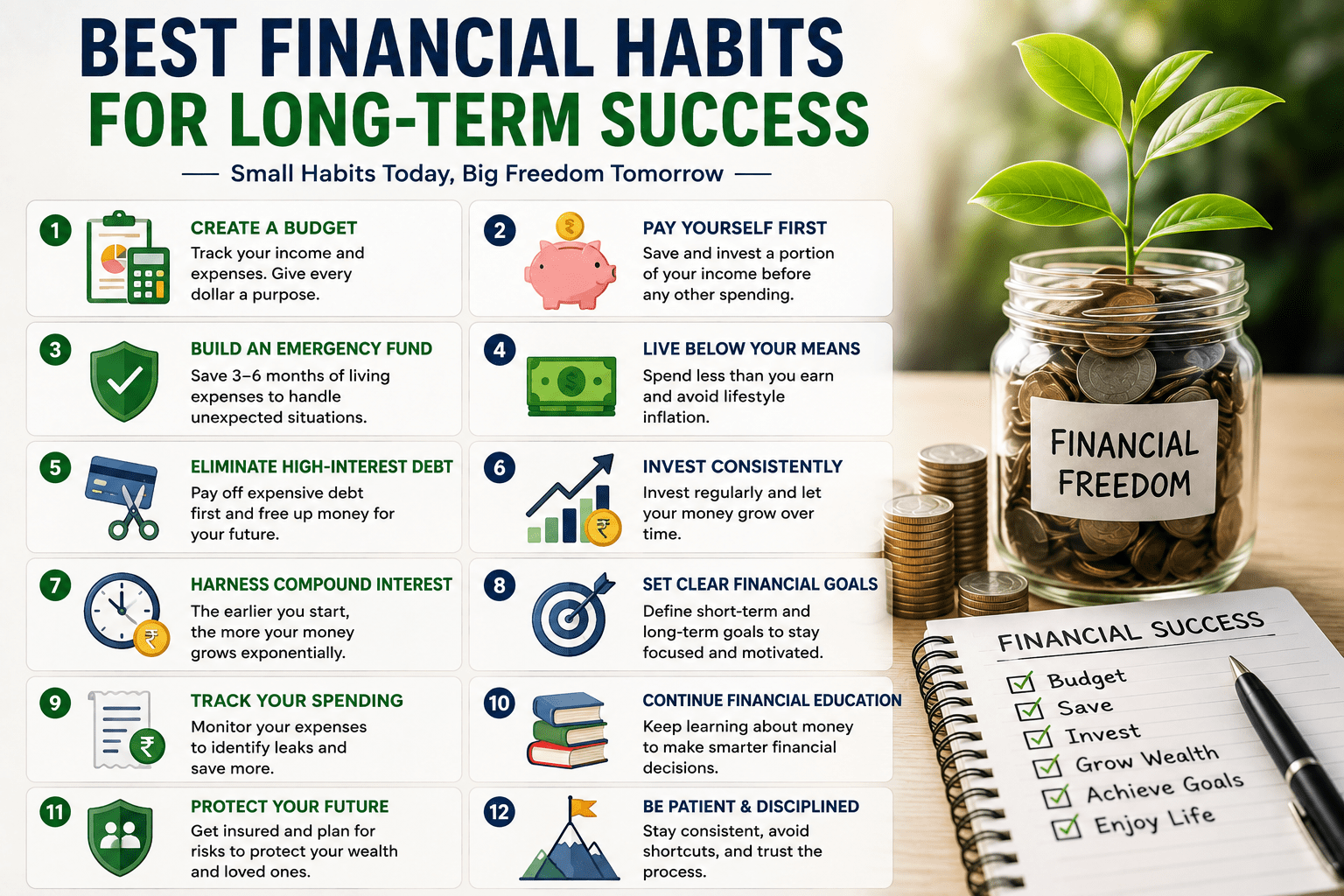

Creating a monthly budget is one of the most effective ways to take control of your finances. Whether you’re saving for a home, paying off debt, building an emergency fund, or simply trying to stop living paycheck to paycheck, a realistic budget provides a clear roadmap for your money.

However, many people abandon their budgets after just a few weeks because they are too restrictive or unrealistic. A budget should be flexible, easy to follow, and tailored to your lifestyle—not something that makes you feel deprived.

In this guide, you’ll learn how to create a monthly budget that actually works, along with practical budgeting strategies, money-saving tips, and common mistakes to avoid.

What Is a Monthly Budget?

A monthly budget is a financial plan that outlines:

- Your monthly income

- Fixed expenses

- Variable expenses

- Savings goals

- Debt payments

- Spending limits

The purpose of a budget is to ensure every dollar has a purpose while helping you avoid overspending.

Why Budgeting Is Important

A well-planned budget helps you:

- Track your spending habits

- Reduce unnecessary expenses

- Save more money consistently

- Avoid debt

- Prepare for emergencies

- Reach financial goals faster

- Reduce financial stress

Budgeting gives you confidence and control over your financial future.

Step 1: Calculate Your Monthly Income

Start by determining your total monthly income.

Include:

- Salary or wages

- Freelance income

- Business income

- Rental income

- Investment income

- Side hustle earnings

If your income varies each month, use the average from the past six to twelve months.

Step 2: List All Monthly Expenses

Write down every expense.

Fixed Expenses

These remain mostly the same each month.

Examples:

- Rent or mortgage

- Insurance

- Loan payments

- Internet

- School fees

- Subscription services

Variable Expenses

These change monthly.

Examples:

- Groceries

- Transportation

- Dining out

- Entertainment

- Shopping

- Utilities

- Fuel

Tracking every expense provides a realistic picture of your spending.

Step 3: Categorize Your Spending

Organize expenses into categories such as:

- Housing

- Transportation

- Food

- Healthcare

- Utilities

- Entertainment

- Savings

- Debt repayment

- Personal expenses

Categorization makes it easier to identify areas where you can reduce spending.

Step 4: Choose a Budgeting Method

Different budgeting systems work for different people.

The 50/30/20 Rule

Allocate your income as follows:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

This method is simple and works well for beginners.

Zero-Based Budget

Assign every dollar of income a specific purpose until your income minus expenses equals zero.

This approach ensures that every dollar is planned and reduces unnecessary spending.

Envelope Budgeting

Set spending limits for categories such as groceries, dining, and entertainment.

Once the allocated amount is spent, stop spending in that category until the next month.

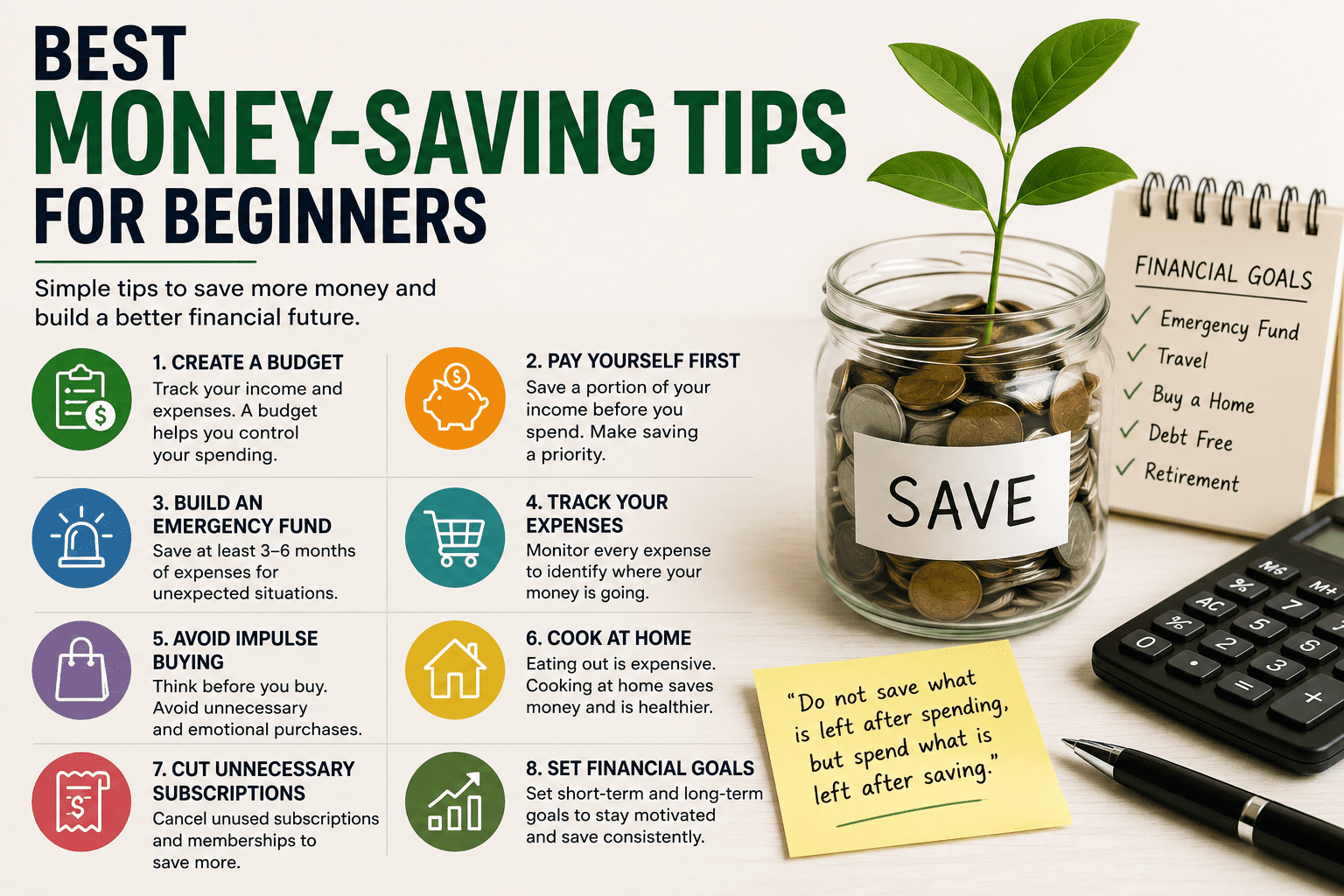

Step 5: Set Financial Goals

A successful budget supports your goals.

Short-term goals may include:

- Building an emergency fund

- Paying off credit card debt

- Saving for a vacation

Long-term goals include:

- Buying a home

- Retirement planning

- Children’s education

- Financial independence

Clear goals help you stay motivated.

Step 6: Build an Emergency Fund

Unexpected expenses happen.

Aim to save at least three to six months of living expenses.

Even starting with a small emergency fund can prevent you from relying on credit cards during emergencies.

Step 7: Track Your Spending

A budget only works if you monitor it regularly.

You can track expenses using:

- Budgeting apps

- Spreadsheets

- Bank statements

- Expense journals

Review your spending weekly instead of waiting until the end of the month.

Step 8: Reduce Unnecessary Expenses

Look for areas where you can cut costs.

Examples include:

- Cancel unused subscriptions

- Cook meals at home

- Limit impulse purchases

- Compare insurance rates

- Reduce energy usage

- Buy generic products

- Shop during sales

Small savings add up significantly over time.

Step 9: Review and Adjust Monthly

Life changes, and so should your budget.

Review it every month to account for:

- Salary increases

- New expenses

- Inflation

- Lifestyle changes

- Financial goals

A flexible budget is much easier to maintain.

Common Budgeting Mistakes to Avoid

Avoid these common mistakes:

- Forgetting irregular expenses

- Setting unrealistic spending limits

- Ignoring small daily purchases

- Not budgeting for entertainment

- Failing to track expenses

- Giving up after one bad month

- Not reviewing your budget regularly

Consistency is more important than perfection.

Best Budgeting Tips for Long-Term Success

To make your budget sustainable:

- Pay yourself first by automating savings.

- Use separate accounts for savings and spending.

- Avoid unnecessary debt.

- Review subscriptions annually.

- Plan meals to reduce food waste.

- Use cashback and rewards wisely.

- Celebrate financial milestones.

Developing good financial habits leads to lasting success.

Budgeting Tools You Can Use

Several tools can simplify budgeting.

Popular options include:

- Budgeting mobile apps

- Spreadsheet templates

- Banking apps with spending insights

- Expense tracking software

- Financial planning calculators

Choose a tool that fits your lifestyle and is easy to use consistently.

Frequently Asked Questions

What is the best monthly budgeting method?

The best budgeting method depends on your financial habits. The 50/30/20 rule is ideal for beginners, while zero-based budgeting offers greater control over every dollar you earn.

How much should I save each month?

A common recommendation is to save at least 20% of your monthly income. However, saving any consistent amount is better than not saving at all.

Why do most budgets fail?

Budgets often fail because they are too restrictive, unrealistic, or not reviewed regularly. A successful budget should be flexible and match your actual lifestyle.

How often should I review my budget?

Review your budget every month and monitor your spending weekly to stay on track and make necessary adjustments.

Can budgeting help pay off debt?

Yes. Budgeting allows you to prioritize debt payments, reduce unnecessary spending, and free up money to pay off loans faster.

Tips for Sticking to Your Budget

- Set realistic spending limits.

- Automate bill payments and savings.

- Avoid emotional spending.

- Keep an emergency fund.

- Review financial goals regularly.

- Involve your family or partner in budgeting.

- Reward yourself for reaching savings milestones.

These habits make budgeting easier and more sustainable.

Conclusion

A monthly budget is more than just a list of numbers—it’s a powerful financial tool that helps you manage your income, control expenses, and achieve your financial goals. By tracking your spending, choosing the right budgeting method, and reviewing your plan regularly, you can create a budget that truly works for your lifestyle.

Remember, the best budget isn’t the strictest one—it’s the one you can consistently follow. Start small, stay committed, and adjust your budget as your financial situation evolves. Over time, smart budgeting will lead to greater financial stability, reduced stress, and long-term wealth.

Also read How AI Is Changing Personal Finance

Leave a Reply