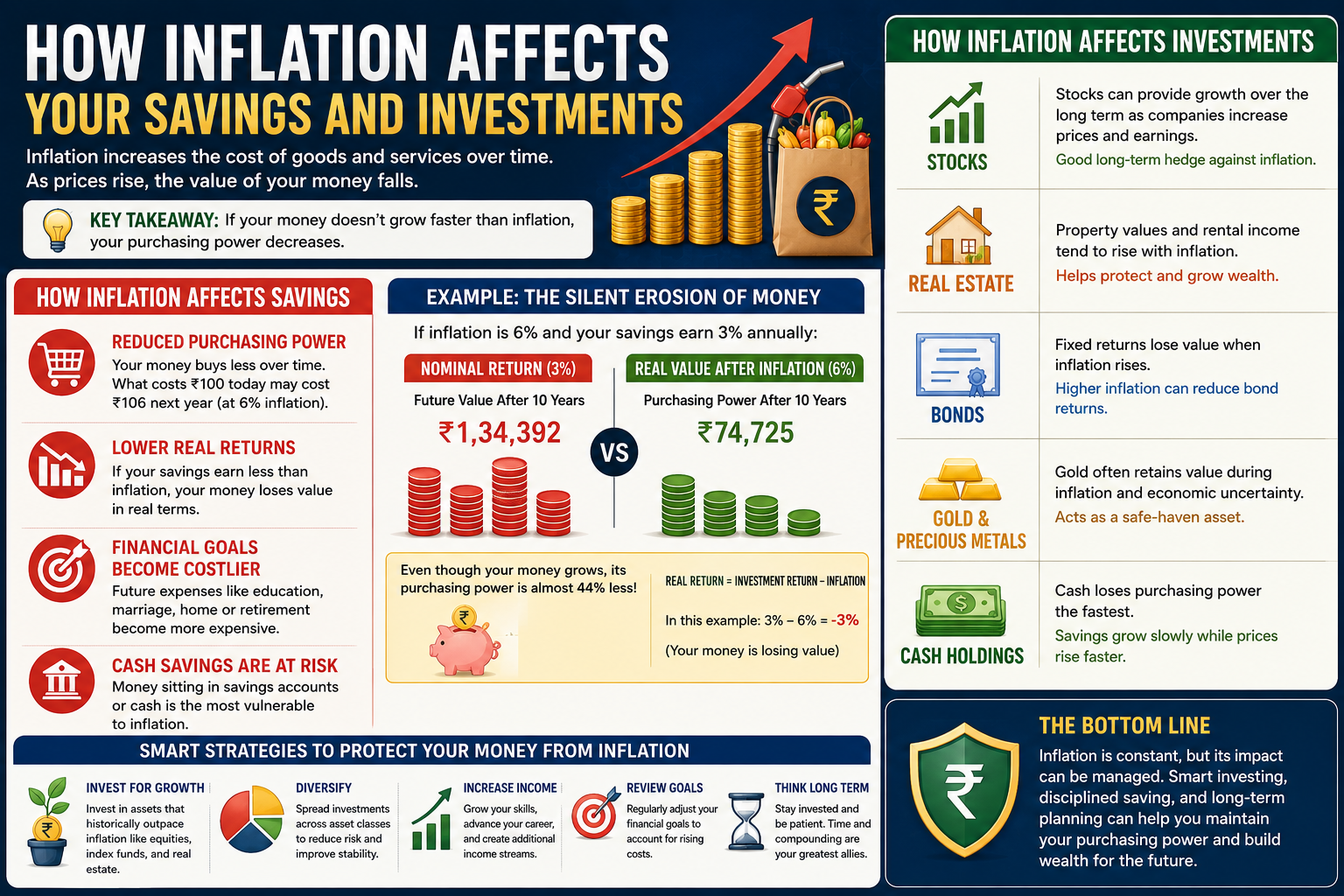

Inflation is one of the most important economic factors that affects personal finances, yet many people underestimate its impact. While inflation may seem like a distant economic concept, it directly influences your purchasing power, savings, investments, and long-term financial goals.

When prices of goods and services rise over time, the value of money decreases. This means the money sitting in your bank account today may buy less in the future if it doesn’t grow faster than inflation.

Understanding how inflation affects your savings and investments can help you make smarter financial decisions and protect your wealth over the long term.

What Is Inflation?

Inflation refers to the gradual increase in the prices of goods and services over time. As inflation rises, each unit of currency buys fewer goods and services than before.

For example:

- A meal that costs ₹200 today might cost ₹220 next year.

- A smartphone worth ₹20,000 today may cost ₹22,000 in a few years.

- Monthly household expenses often increase due to inflation.

While moderate inflation is a normal part of a healthy economy, high inflation can significantly impact personal finances.

Why Inflation Matters

Inflation affects everyone because it reduces purchasing power.

Example

Suppose you have ₹100,000 in a savings account earning 3% annual interest.

If inflation is 6%, your money is technically growing, but its purchasing power is shrinking.

This means:

- Savings grow by 3%

- Prices rise by 6%

- Real purchasing power decreases by approximately 3%

This is why simply saving money is often not enough.

How Inflation Affects Your Savings

1. Reduced Purchasing Power

The most direct effect of inflation is that your money buys less over time.

For example:

- Groceries become more expensive.

- Fuel costs increase.

- Healthcare expenses rise.

- Housing prices climb.

If your savings are not growing at a rate that matches inflation, your wealth effectively declines.

2. Lower Real Returns

Many traditional savings accounts offer relatively low interest rates.

If inflation exceeds your savings account’s interest rate, your real return becomes negative.

Formula for Real Return

Real Return≈Investment Return−Inflation Rate

For example:

- Savings Account Return = 4%

- Inflation Rate = 6%

Real Return = -2%

Even though your account balance grows, your purchasing power decreases.

3. Longer Time Needed to Reach Financial Goals

Inflation can make future goals more expensive.

Examples include:

- Buying a home

- Funding education

- Starting a business

- Retirement planning

A goal that costs ₹10 lakh today may require significantly more money in the future.

How Inflation Affects Investments

While inflation negatively impacts cash savings, its effect on investments varies depending on the asset class.

1. Stocks

Stocks have historically been one of the best long-term defenses against inflation.

Companies often raise prices during inflationary periods, which can increase revenues and profits.

Benefits include:

- Potential capital appreciation

- Dividend income

- Long-term growth

However, short-term market volatility may increase during periods of high inflation.

2. Real Estate

Real estate often performs well during inflation.

Property values and rental income tend to increase as prices rise.

Advantages include:

- Potential appreciation

- Rental cash flow

- Inflation protection

Many investors view real estate as a hedge against inflation.

3. Bonds

Inflation can negatively affect traditional bonds.

Why?

Fixed bond payments lose purchasing power when prices rise.

For example:

A bond paying 5% annually becomes less attractive if inflation rises to 7%.

This reduces the real return received by investors.

4. Gold and Precious Metals

Gold has long been considered an inflation hedge.

Investors often turn to gold during periods of economic uncertainty because it tends to retain value over time.

Benefits include:

- Wealth preservation

- Diversification

- Protection during inflationary periods

However, gold does not generate income like stocks or real estate.

5. Cash Holdings

Cash is generally the most vulnerable asset during inflation.

Money kept in:

- Savings accounts

- Checking accounts

- Physical cash

may lose purchasing power if inflation exceeds interest earnings.

The Impact of Inflation on Retirement Savings

Inflation is particularly important when planning for retirement.

Many people underestimate how much future expenses will increase.

Example

If annual living expenses are ₹500,000 today, they may be substantially higher in 20 or 30 years due to inflation.

Retirement planning should account for:

- Rising healthcare costs

- Increased living expenses

- Longer life expectancy

Investments must generate returns that exceed inflation to maintain purchasing power.

Strategies to Protect Your Wealth From Inflation

1. Invest Rather Than Rely Solely on Savings

While emergency savings are important, keeping all your money in cash can limit long-term growth.

Consider investing in:

- Stocks

- Index funds

- Mutual funds

- Real estate

These assets often provide returns that outpace inflation over time.

2. Diversify Your Portfolio

Diversification helps reduce risk and improve long-term stability.

A diversified portfolio may include:

- Equities

- Bonds

- Real estate

- Precious metals

- Cash reserves

Different asset classes respond differently to inflation.

3. Increase Income Over Time

One of the best ways to combat inflation is by increasing your earning potential.

Strategies include:

- Career advancement

- Skill development

- Side businesses

- Freelancing

- Passive income streams

Growing income helps offset rising living costs.

4. Review Financial Goals Regularly

Financial goals should be adjusted periodically to account for inflation.

Review:

- Savings targets

- Retirement plans

- Education funds

- Major purchase goals

Updating goals ensures you remain on track.

5. Focus on Long-Term Investing

Trying to predict short-term inflation trends can be difficult.

Instead:

- Invest consistently

- Stay diversified

- Maintain a long-term perspective

Historically, long-term investing has been one of the most effective ways to overcome inflation.

Common Mistakes People Make During Inflation

Avoid these common errors:

- Keeping excessive cash reserves

- Panic selling investments

- Ignoring rising living costs

- Failing to adjust financial goals

- Chasing high-risk investments

- Neglecting diversification

Making informed decisions helps preserve wealth during inflationary periods.

Inflation and the Power of Compound Growth

While inflation reduces purchasing power, compound growth can help offset its effects.

Investments that consistently generate returns above inflation can significantly increase wealth over time.

The key is to:

- Start early

- Invest consistently

- Stay patient

- Focus on long-term growth

These habits can help maintain and increase your purchasing power.

Conclusion

Inflation is an unavoidable part of the economy, but it doesn’t have to derail your financial goals. Understanding how inflation affects your savings and investments allows you to take proactive steps to protect your wealth.

While inflation can reduce the value of cash savings, strategic investing, diversification, and long-term financial planning can help maintain and grow your purchasing power. By making informed financial decisions today, you can build a stronger and more resilient financial future.

Also read Best Investment Strategies for Young Professionals

Leave a Reply