Managing your money effectively is one of the most important skills you can develop. Yet many people struggle with budgeting because they either don’t know where to start or find it difficult to stay consistent. Learning how to create a budget and stick to it can help you take control of your finances, reduce stress, and achieve your financial goals faster.

A well-planned budget allows you to understand where your money is going, identify unnecessary expenses, and make smarter financial decisions. Whether you’re saving for a house, paying off debt, building an emergency fund, or simply trying to improve your financial health, budgeting is the foundation of success.

In this guide, you’ll learn practical steps to create a budget that works and strategies to stay committed to it over the long term.

What Is a Budget?

A budget is a financial plan that outlines your income and expenses over a specific period, usually monthly. It helps you allocate your money toward essential expenses, savings, debt payments, and personal spending while ensuring you don’t spend more than you earn.

Think of a budget as a roadmap for your finances. Without one, it’s easy to overspend and lose track of your financial goals.

Why Budgeting Is Important

Creating and following a budget offers numerous benefits, including:

- Better control over your finances

- Reduced financial stress

- Increased savings

- Faster debt repayment

- Improved spending habits

- Better preparation for emergencies

- Greater financial security

A budget gives every dollar a purpose, making it easier to manage your money responsibly.

Step 1: Calculate Your Monthly Income

The first step in creating a budget is understanding how much money you bring in each month.

Include all income sources such as:

- Salary or wages

- Freelance income

- Business earnings

- Rental income

- Investment income

- Side hustles

Use your after-tax income rather than your gross income to get a more accurate picture of the money available for spending and saving.

Step 2: Track Your Expenses

Before creating a budget, you need to know where your money currently goes.

Review your spending over the last two or three months and categorize expenses into:

Fixed Expenses

These costs remain relatively consistent each month.

Examples include:

- Rent or mortgage

- Insurance premiums

- Loan payments

- Internet bills

- Subscription services

Variable Expenses

These expenses change from month to month.

Examples include:

- Groceries

- Dining out

- Entertainment

- Transportation

- Shopping

Tracking expenses helps identify spending patterns and areas where you can reduce costs.

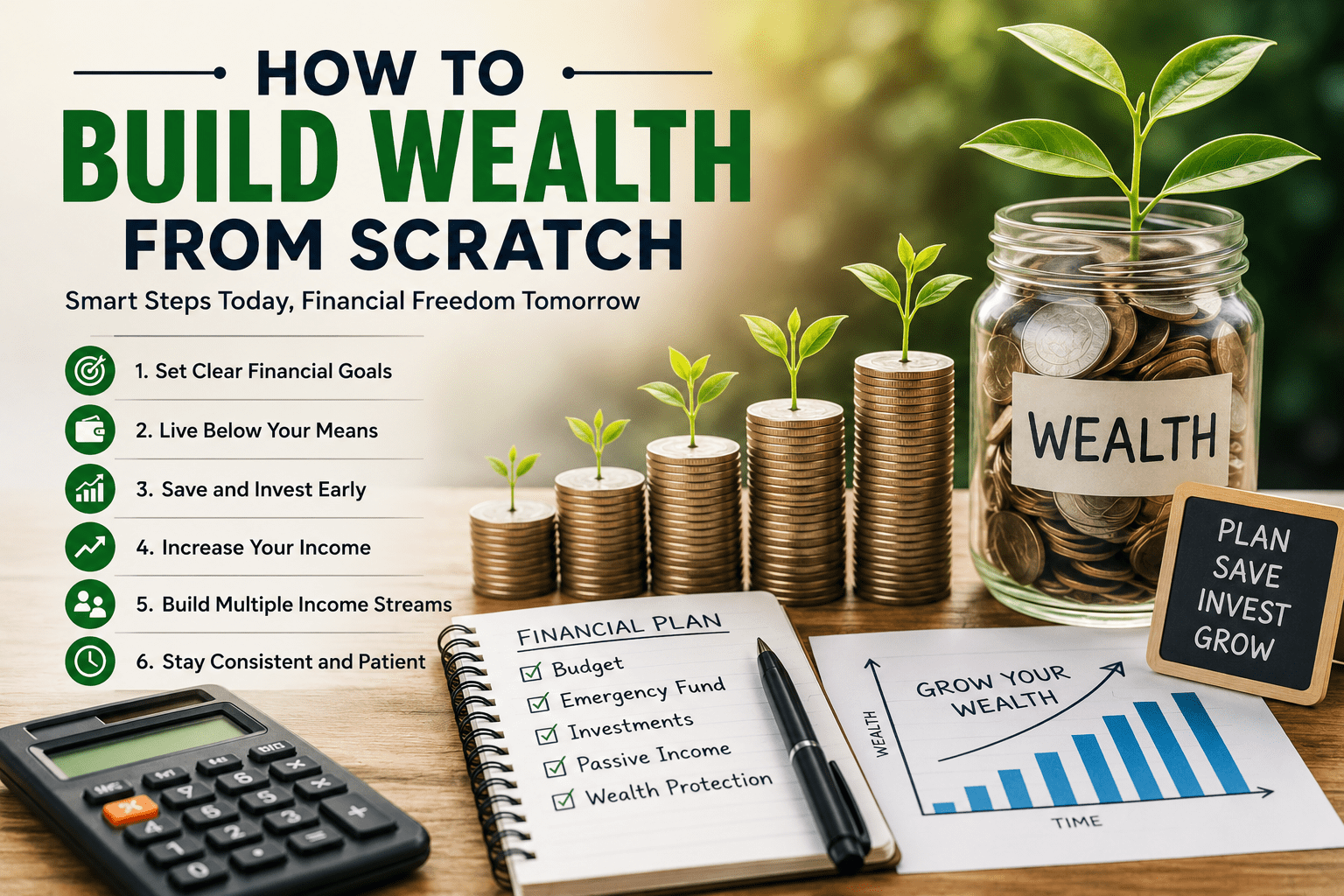

Step 3: Set Financial Goals

A budget becomes more meaningful when it supports specific financial goals.

Common goals include:

Short-Term Goals

- Building an emergency fund

- Paying off credit card debt

- Saving for a vacation

- Buying a new gadget

Long-Term Goals

- Purchasing a home

- Retirement planning

- Funding education

- Achieving financial independence

Having clear goals increases motivation and makes sticking to your budget easier.

Step 4: Choose a Budgeting Method

There are several budgeting systems available. Choose one that fits your lifestyle and financial situation.

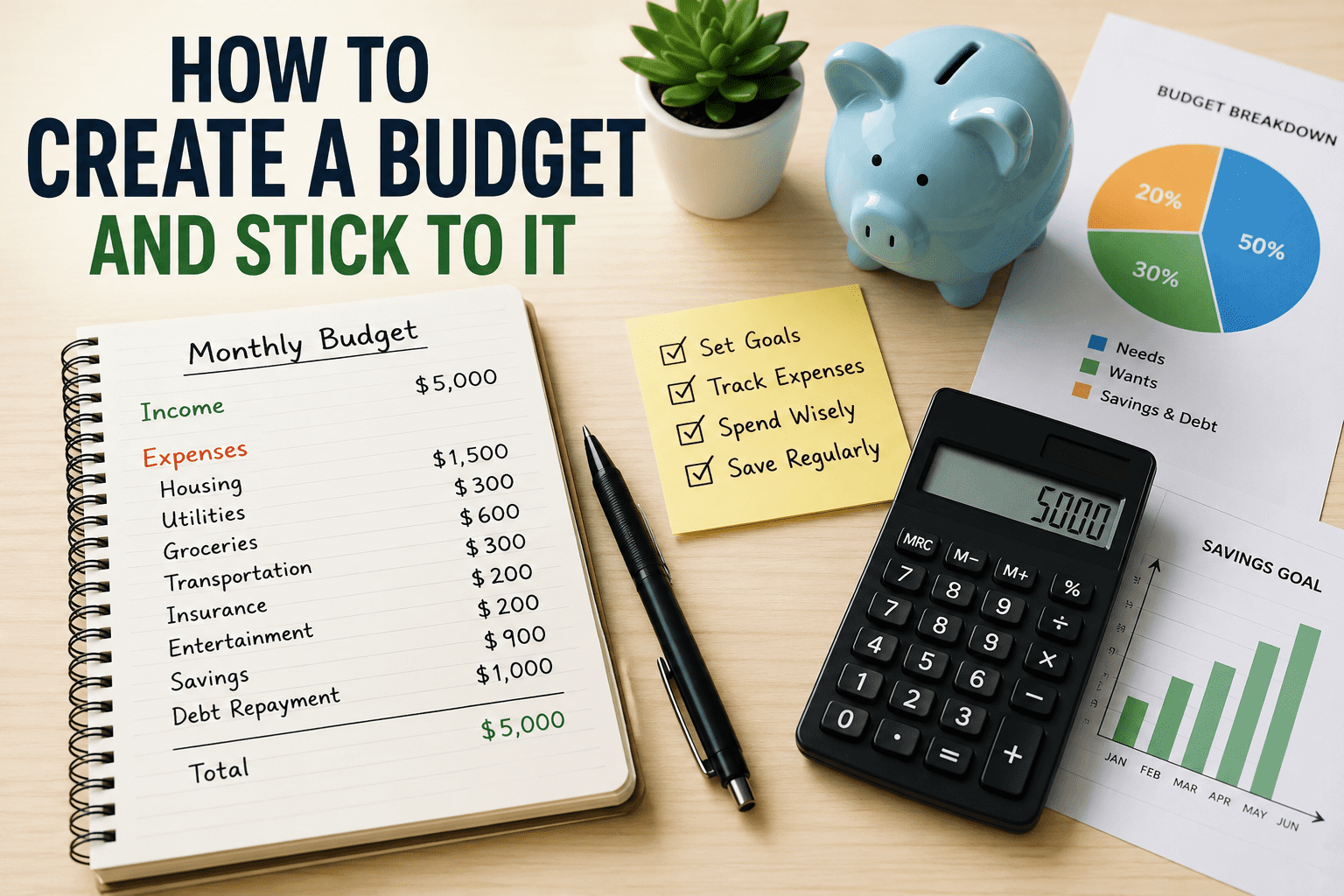

The 50/30/20 Rule

This popular budgeting method divides your income into three categories:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

This approach is simple and ideal for beginners.

Zero-Based Budgeting

With zero-based budgeting, every dollar is assigned a purpose until your income minus expenses equals zero.

This method provides maximum control over spending.

Envelope Budgeting

You allocate specific amounts of cash to different spending categories using envelopes.

Once an envelope is empty, spending in that category stops until the next budgeting period.

Step 5: Create Your Monthly Budget

Now it’s time to build your budget.

Start by listing:

- Total monthly income

- Essential expenses

- Savings contributions

- Debt payments

- Discretionary spending

Ensure your total expenses do not exceed your income.

If expenses are too high, identify areas where you can cut back.

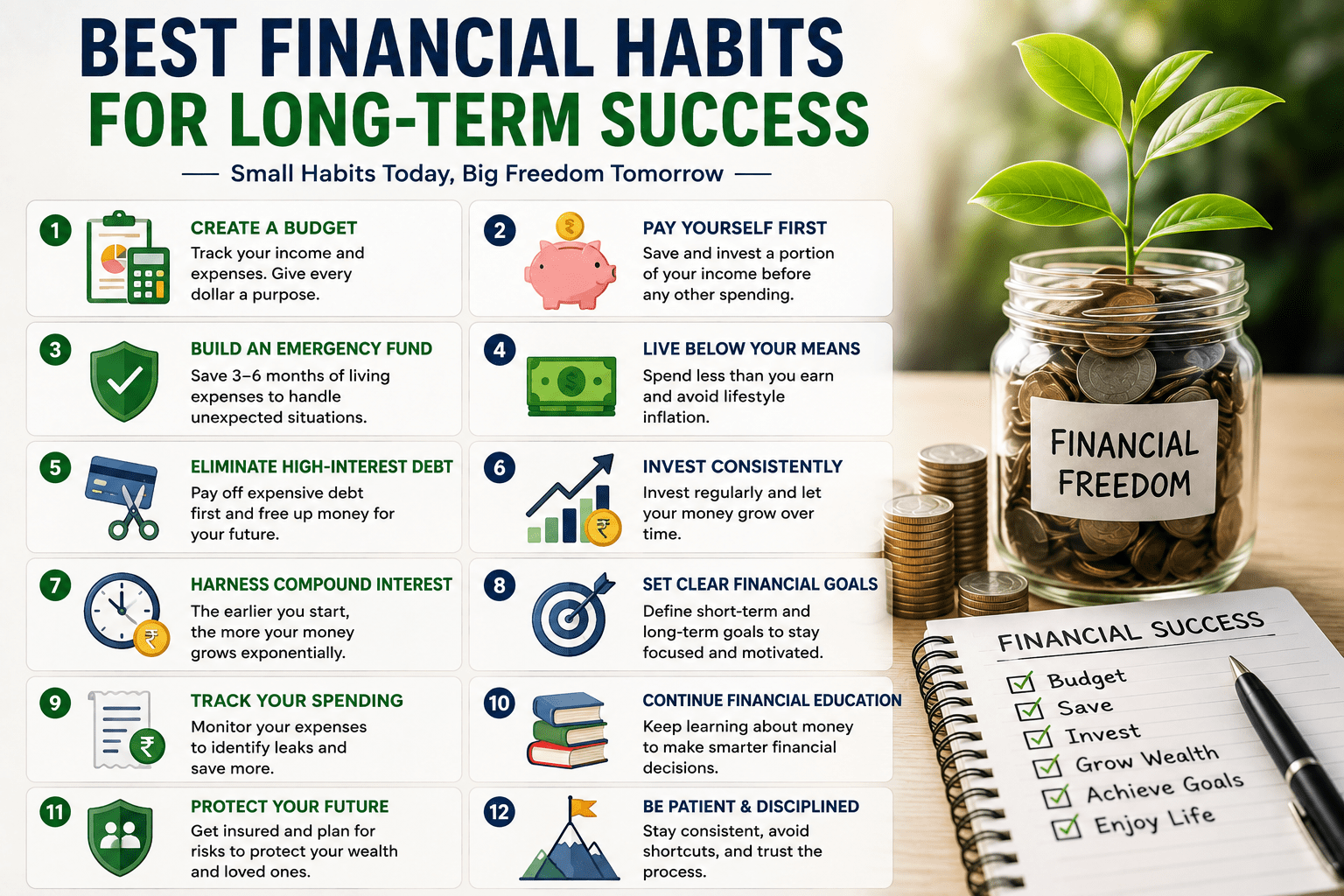

Step 6: Prioritize Saving

Many people make the mistake of saving whatever money remains at the end of the month.

Instead, treat savings like a regular bill.

Consider automating transfers to:

- Emergency funds

- Retirement accounts

- Investment portfolios

- Goal-specific savings accounts

Paying yourself first helps build wealth consistently.

Step 7: Monitor Your Spending Regularly

A budget is not something you create once and forget.

Review your finances weekly or monthly to ensure you’re staying on track.

Use budgeting tools and apps to:

- Track spending

- Monitor account balances

- Set financial goals

- Receive spending alerts

Regular monitoring allows you to make adjustments before small issues become major problems.

Common Budgeting Mistakes to Avoid

Setting Unrealistic Goals

Creating an overly restrictive budget often leads to frustration and failure.

Allow room for occasional entertainment and personal spending.

Ignoring Small Expenses

Daily coffee runs, online subscriptions, and impulse purchases may seem insignificant but can add up quickly.

Not Preparing for Emergencies

Unexpected expenses are inevitable.

Include an emergency fund in your budget to avoid relying on debt.

Failing to Adjust Your Budget

Life circumstances change.

Review and update your budget regularly to reflect changes in income, expenses, and financial goals.

Tips to Stick to Your Budget

Automate Financial Tasks

Automate bill payments and savings transfers to reduce the risk of missing payments or forgetting to save.

Use Cash for Problem Spending Areas

If you tend to overspend in certain categories, using cash can help limit spending.

Track Progress Toward Goals

Seeing your savings grow or debt decrease can be highly motivating.

Reduce Temptations

Unsubscribe from promotional emails and avoid unnecessary shopping trips.

Reward Yourself Occasionally

Celebrate financial milestones with affordable rewards to maintain motivation.

Budgeting Tools and Apps

Several budgeting apps can simplify money management.

Popular options include:

- Mint

- YNAB (You Need A Budget)

- PocketGuard

- EveryDollar

- Goodbudget

These tools help track spending, create budgets, and monitor financial progress efficiently.

The Long-Term Benefits of Budgeting

When practiced consistently, budgeting can transform your financial life.

Benefits include:

- Increased savings

- Reduced debt

- Better financial discipline

- Greater peace of mind

- Improved financial confidence

- Faster achievement of financial goals

The earlier you start budgeting, the greater the long-term rewards.

Conclusion

Learning how to create a budget and stick to it is one of the most effective ways to improve your financial future. A budget provides clarity, helps control spending, supports savings goals, and reduces financial stress. By tracking your income and expenses, setting realistic goals, choosing the right budgeting method, and reviewing your finances regularly, you can develop healthy money habits that last a lifetime.

Remember that budgeting is not about restricting your life—it’s about making intentional decisions with your money. With consistency and discipline, a well-structured budget can help you achieve financial stability and long-term success.

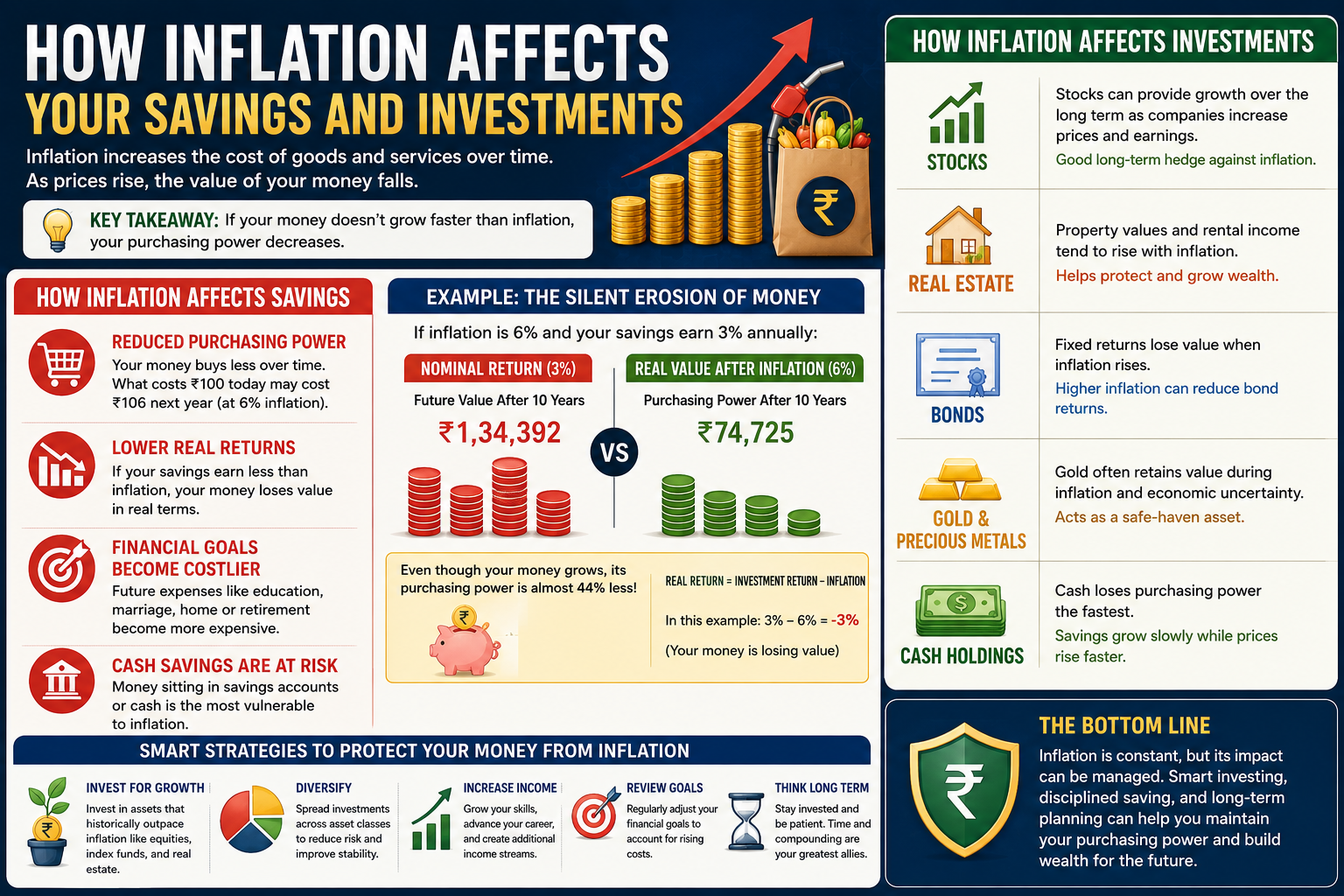

Also read How Inflation Affects Your Savings and Investments: A Complete Guide

Leave a Reply